I’ll kick off this piece with some charts. The first one is historical inflation in the US, UK, Japan, Germany and France (1950-1994).

The exact numbers aren’t important – what catches my eye is two periods (early 50s & mid-70s) where inflation was at, or over, 7.5% per annum for a few years. To see why this matters, let’s do a case study.

You have $1,000 stashed in your mattress (or yielding close to 0% in a bank account). Across the year, prices go up by 2.5%. With the gradual increase in prices, how does the effective value of your money change over time?

I view inflation like a negative interest rate. Instead of earning money across the year, you “lose” money because your purchasing power goes down.

In our example, $1,000 on January 1st would buy the equivalent of $975.61 on December 31st.

$1,000 divided by (1 + inflation rate)

You can’t buy as much a year later because prices went up, and you didn’t earn anything on your money.

To be able to buy the same amount of stuff, you would need an after tax return of 2.5%. When your investment return is equal to the inflation rate, you stay neutral. In our example, $1,000 times (1+0.25) = $1,025 is required to stay neutral on December 31st.

Real Return = After Tax Return minus Inflation Rate

Most people will feel happy when $1,000 goes to $1,025 over a year. However, in our example, you haven’t moved forward. Your return has let you stay in the same place.

Right now, the return on low-risk assets is small and the inflation rate is small. So parking your money in low-risk / low-return assets has little cost to your purchasing power. However, doing this for many years can be a poor investment strategy. Inflation hurts consumers slowly and, aside from the price of gas, is largely hidden from our collective consciousness.

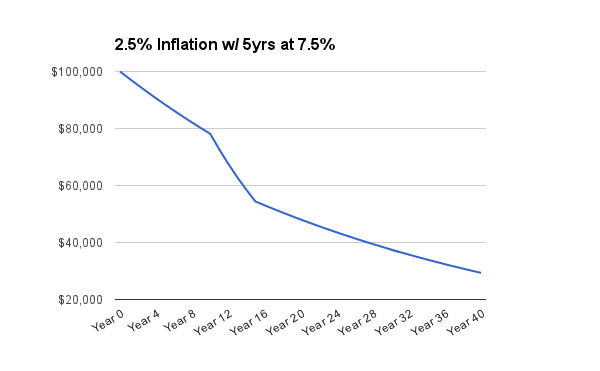

Consider the chart that follows – it assumes a baseline inflation rate of 2.5% per annum and a five-year block where inflation jumps to 7.5%.

The chart shows the purchasing power of $100,000 over time. I used $100,000 because that’s the target that I’m going encourage my kids to achieve by the time they’re 30. It’s do-able if they save $20 per day from the time they are 18.

When my balance sheet was largely low-risk, low-return cash equivalent assets, the chart (above) was on my mind. The steep drop in purchasing power due to a five-year period of higher than average inflation would hurt my family’s purchasing power. With extremely low interest rates and rapid Central Bank money creation, I thought (incorrectly) that significant inflation was right around the corner.

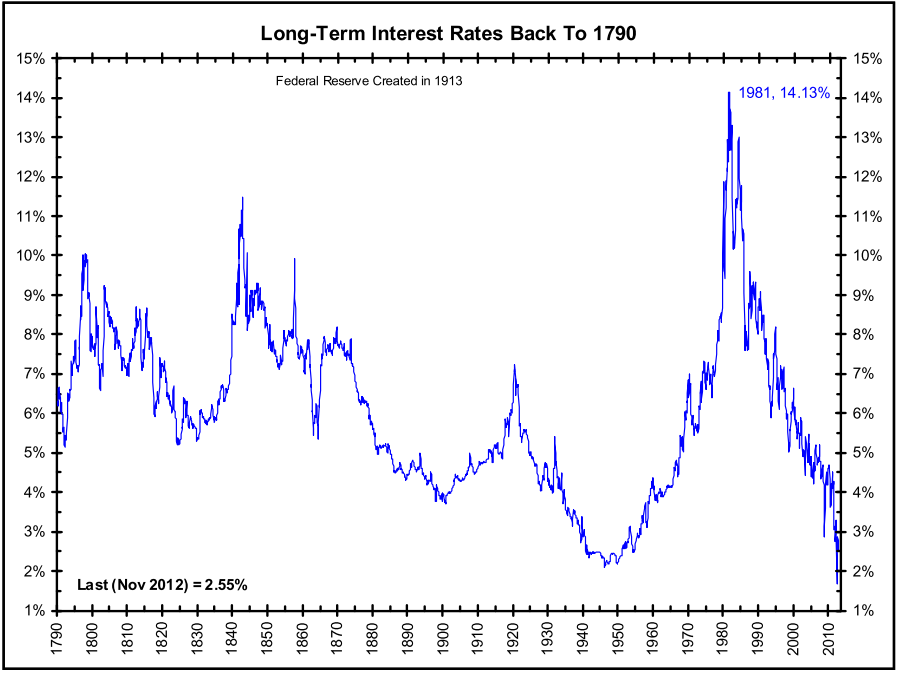

How low are today’s rates? The chart below (posted yesterday by Ritholtz’s blog) gives an idea. Note that the chart goes back to 1790.

In 2009/2010, I made a decision to shift into real estate. The market was falling and debt finance wasn’t available. For me, it was the perfect time to buy and I expected Boulder real estate to hold its real purchasing power. In other words, I expected the long-term value of my investment to link closely to the inflation rate. I wasn’t trying to get rich, in a very uncertain time, I wanted an investment that was likely to hold purchasing power. We hear this argument about gold but gold lacks many of the benefits of residential real estate. For an explanation of long-term real estate valuation see Shiller – Irrational Exuberance.

For what it’s worth, an alternative investment that I considered was buying two large-cap stocks (GE/WMT) with attractive dividend yields. I wasn’t able to achieve my target entry price on the stocks so missed that window.

In addition to an expectation that real estate would hold its real purchasing power, the net yield on real estate is attractive if interest rates fall to very low levels. Real estate offers some income protection against prolonged very low inflation and even lower interest rates. I didn’t expect rates to fall as far as they did but considered “what if.”

Here’s a chart that plots US rates against the post-bubble history in Japan:

The precise numbers aren’t important. What’s useful is to consider a scenario where low-risk assets have yields under 1% for five, or more, years. What type of investments make sense in that environment? For me, high-quality real estate makes sense. There’s a substantial section in my latest book about real estate.

Other investments that make sense are my kids 529 college accounts and low-cost index funds. The 529 program that we use is has a 0.46% expense ratio and is tax-free, or tax-deferred, depending on use of funds. In 2012, I started small, weekly investments in Vanguard funds for my kids. With Vanguard, the index products (VTSAX/VTIAX) have expense ratios of 0.06% and 0.18% respectively. I’ve only used the US fund so far but am considering adding international.

The index funds have yields that are lower than what I earn on real estate but they are far easier (and less costly) to sell.

My point: inflation can be a risk, or a benefit, to your family finances. When thinking about portfolio strategy, consider how changes in inflation, and interest rates, will impact your life. Be comfortable with every scenario and remember that we are in a highly unusual situation.

Next week I’ll share a case study of using a mortgage to protect your family from unexpected inflation. I think it’s a much more practical strategy than speculating in commodities, like gold.