When I left my private equity career in 2000, I was able reduce my annual expenditure 90% by moving from Hong Kong to New Zealand. I bought a five-bedroom house for US$25 per sq ft (those were the days) and the income from that property covered my housing expenses. Kiwi health care is government funded and I purchased a top-up policy for my travels.

At the time, my Dad advised me to “take the number that you think you need to retire and triple it.” In 2000, I had neither the desire to retire nor a particular number in mind. His advice proved accurate as I gained clarity on what’s required for me to retire, at any given point.

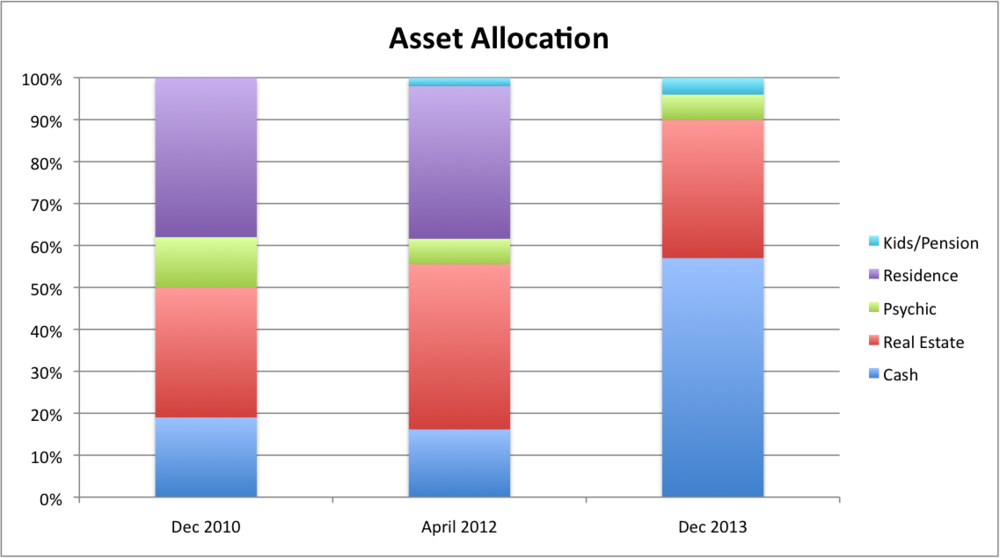

The last time I wrote about asset allocation was December 2010. I shared that my split was 50:50 between assets with postive returns (investments) and assets that had a psychic return. A psychic return is another way of saying the assets depreciate, or cost me money to hold.

Like most people, our house is the largest asset in the family’s balance sheet and the true cost of that asset has been weighing on me. I’ve decided to scratch the itch, sell the house, free the family from being tied to any one location and reallcoate the capital to something productive. It’s been a fascinating study of human psychology as I’ve been living through my biases.

Right now, we are in the middle column transitioning towards a more liquid position. The pain that we take is leaving our existing house. The benefit, of improved financial health, is invisible to my wife and kids. My daughter’s main concern is bringing the cats to any new residence, so I have her covered.

The other major change I have started is allocating capital for my kids’ education, they have 529 accounts, which let gains roll up tax free. I made an error when we started saving for the kids by using a minor custody account, rather than the 529 vehicles. Both the kid’s accounts invest in a low-cost index fund of US equities. I’ve taken a twenty-year view of the markets on their behalf.

Over the last three years, I made a decision to allocate the family’s earned income to a business owned by my wife. This enabled us to start a 401k for her and get her credit rating established. A project for 2012-2013 is setting me up in a similar fashion.

The kids/pension allocation will likely tick up by 2% per annum and be mainly allocated to equities. In a high tax, high rate environment, previous allocations into tax deferred vehicles will be valuable.

I lifted the above chart from Barry Ritholtz’s Blog. Ever since I saw that chart, I’ve been asking myself where I want to be when conditions shift back to normal. Conditions are going to shift eventually and we, collectively, give too much weight to the last three years of extremely low rates.

I’m shifting to cash equivalents to give myself the choice to spend that money (gradually) while I allocate more time to my family and wait for conditions to return to normal. Also, that gives me the flexibility to move quickly if there is another unpleasant shock. My property portfolio was purchased in a four month period when conditions suited me.

I’m willing to foresake a lot of upside, and endure considerable hassle/pain from moving, so that I can be relaxed around the house and have time to love, write and ride.

There’s a leap of faith that I’m going to forget the current pain in a few years time. I enjoy reading old blogs so this is a reminder to myself to check back in.