I had a friend ask me if I thought “cash is king” in the current environment. My answer is more than can fit in a tweet so here you go.

Key Point: when we read reports of monetary policy tightening, I think we are being misled. On a historical basis, policy remains accommodating.

The collective is lousy at remembering history.

US Federal Reserve Total Assets

The value of everything, in the world, has been inflated by the actions of Central Bankers. I think everyone accepts that point. Thing is, it is impossible to measure the scale of the inflation.

In recent memory, the best example will be to cast your mind back to when crypto was a one-way bet.

Asset inflation feeds upon itself, until it doesn’t.

The increase in the size of the Fed’s balance sheet has been a strong tailwind and dominates our collective memory.

If you’re 35 and under, then unprecedented monetary inflation is the only environment you’ve ever known.

Time for another chart.

As at 12 Sept 2022

Here’s a chart of our current reality (black line).

We’ve lived the rate increase, but assets prices have not adjusted to the new reality.

Why?

The economy is rolling along – the tailwind was powerful, and strong

It is unclear where the Fed’s massive balance sheet is going – there has been 13 years of QE – who wants to bet against another round, I don’t

There remains plenty of OPM (other people’s money) and leverage

Those are equity, bond and money market funds I track, as at last Monday.

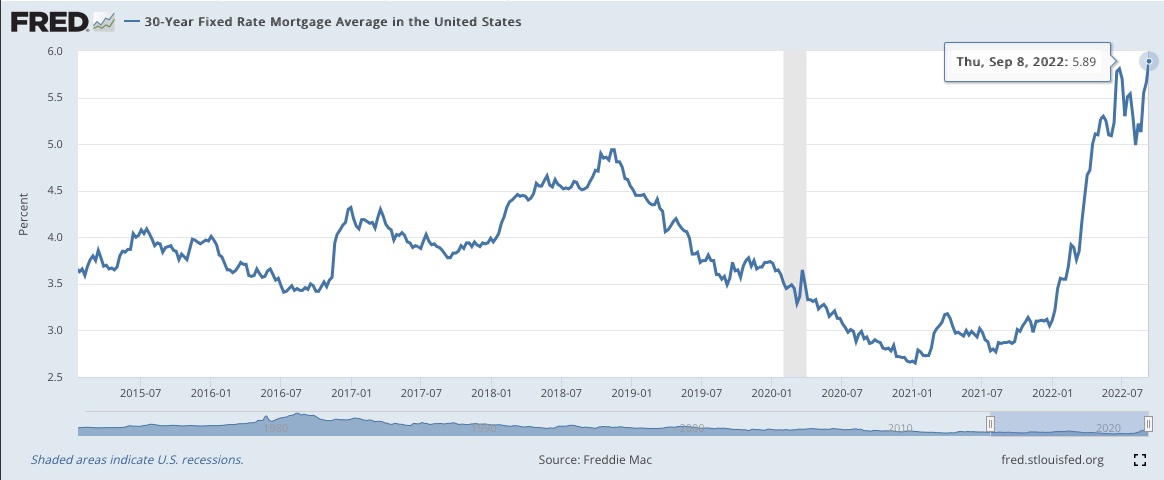

US 30-year Mortgage Rates 2015-now

Mortgage rates appear to have jumped.

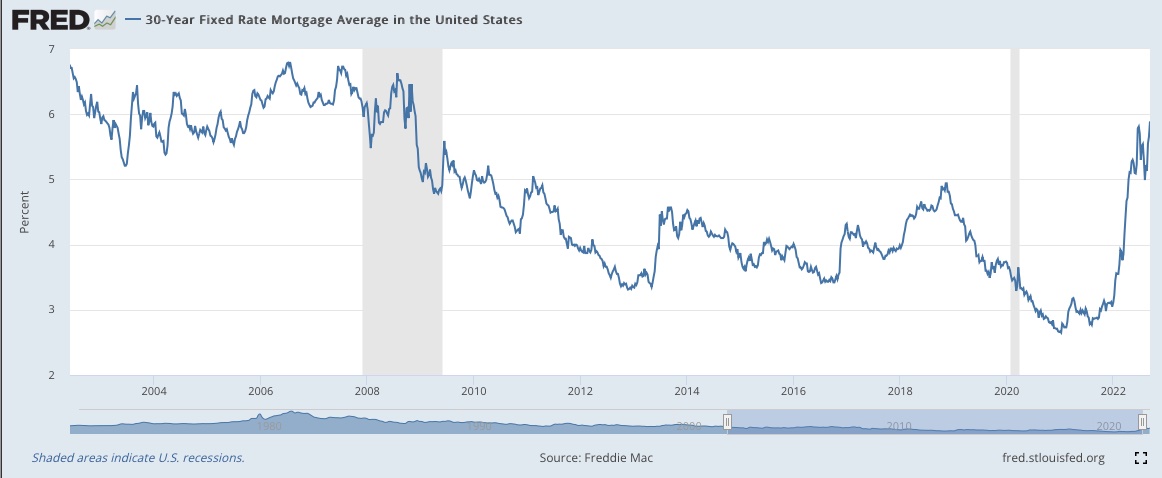

However, let’s have a look at the next chart.

2003-now

Rates are only just getting back to their 2003-2008 level, a time when people were hardly holding back on real estate.

So what do I think:

1// Assets could get cheaper – I don’t see any case for a melt up.

2// If the Fed materially shrinks their balance sheet then assets will get a lot cheaper. Cutting their balance sheet in half takes us back to 2015.

3// Sit down and ask yourself “what if” asset prices drop to 2015 levels, a 50% reduction. Odds are, you have your interest rates locked in. So the main risk will be short term cash flow due to unemployment. How might you protect yourself?

4// Having a year’s core cost of living in an “emergency” fund makes sense. Personally, I didn’t reinvest the proceeds from a Q2 asset sale. My reserve is enough to navigate a nasty recession without selling anything further.

So a “prudent cash reserve” is King.

I don’t think it makes sense to liquidate positions, and pay extra taxes, because risk assets might fall in value.

Feels like I’m getting to the end of my Thursday finance series!

Things I’ve noticed in May 2022:

Stablecoin instability

Pain at the retail level

Step-down price adjustments of stable businesses with mkt cap >$1 billion (disappearance of margin trade on reliable dividends, perhaps)

Buyer of my sale was 95% debt financed with a payment of 3x the gross rent I was receiving

Market down 19%, as I write

What I haven’t seen:

Widespread pain

Institutional capital destruction

Anything, anywhere, that looks cheap

Given the money creation of this cycle, those are key words to watch:

Pain

Capital Destruction

Cheap

Until those arrive, I’m going to be patient and live my life.

A reminder.

The Great Recession of 2008/2009 first got my attention with trouble in the interbank lending market (Early Summer 2008), this was after ~20% market decline.

There was a long way for the bear market to go, and its effect on real asset prices had years to run.

Great deals were available 2010-2012 => the equivalent of 2-4 years from “now”

Same thing in the UK Recession of 1990, my first out of school.

If we’re in a blip then rebalancing will be just fine

If we’re in for something more serious then it takes time to develop AND it takes years for price expectations to adjust

Teach your kids their financial lives will be about no more than a dozen choices.

Here are mine:

Study finance (class of 1990)

Save 50% of my take home (1990-2007)

Partners investment scheme (late 90s, all in then, equivalent of 1 yr spending now)

Work to build a startup (2000)

Sell into the frenzy (2005-2007)

Move into a low-cost Vanguard portfolio (2008 onwards)

Boulder real estate (2010 & 2012))

Downsize (2012-2013)

Borrow long at 3.25% (2013)

Debt free (2007 & 2020)

Have kids with a kind woman from a humble background (on going)

Every other choice turned out to be noise. What to do?

Focus on actions, not outcome.

What does that really mean?

Do what moves you forward and have faith. Sport, marriage, money, all things… daily action is the fundamental force moving you towards “better.”

Education matters => I was given a chance in Private Equity because I had high marks in a useful field. Between my high school graduation (1986) and my youngest’s (2031) the nature of “useful” will have changed. However, the need for skilled people to “do” will endure.

The most useful part of my degree wasn’t finance! It was financial accounting, programming and mathematics => I learned fundamental knowledge in college. I learned my profession on-the-job. You learn the valuable part by doing work, for the best people you can find.

This keeps popping up over and over again (professors, partners, coaches, mentors, twitter follows). At 53, I’m learning from people less than half my age! Do work to learn.

Avoid Ruin => studying, then working in, financial accounting helps you learn when a situation doesn’t feel right. Embezzlement is an old game and it’s useful to learn the patterns. Financial fraud happens, and will continue to happen. Take steps to reduce your family’s exposure to ruin.

With the accounting, I learned the most with 9 credits spread across three courses. Financial Accounting 1, 2 and 3. Small investment, huge return. Do it when you’re young. Being forced to rely on others to do your financial math is a disadvantage that will cost you.

Let’s pull it together for you…

Starting your working life (in a useful field, with your financial accounting courses done)…

Waiting for the fat pitch – once in a lifetime investment opportunities happen once a decade

Turning yourself into the sort of person you’d like to marry, the friend you’d like to have, the parent you aspire to be => meaningful connection is true wealth

Your mind will try to trick you into thinking it’s the investment choices that matter.

It is not.

It is the four habits I outlined above, and avoiding substance abuse.

Fortune’s Formula by Poundstone was recommended inside Safe Haven. The book touched on a number of questions/issues I’ve been pondering since attending Taleb’s seminar in October 2019.

Very helpful book!

What follows are a bunch of points I’m writing down so I can refer back later.

Insurance proceeds: Will I be able to access my money when I need it? Applies to everything, especially exotics.

All families are sellers, eventually.

This is an important point because crashes are most damaging when one is forced to sell into them. Ironic point is many (most?) of us choose to sell into them (or in fear of them).

Recently, I came across an article about CalPERS selling billions into a dip – even smart people make poor decisions, most often when they are custodians of other people’s money.

Most institutions have shorter memories than families. Keep reminding yourself of your mistakes – you probably paid a lot to learn your lessons.

Train yourself, and your kids, to be able to tolerate bad news. It saves time, money and emotion.

Counter-party Risk

Payout => who’s on the other side of my insurance trade and are they going to need a bailout to pay me? If my insurance company might need a bailout then am I really insured?

I’ve done my best deals when all buyers have disappeared. A delay in payout can have a huge opportunity cost to me.

Skill => reading financial history, I notice the people on the other side have… better analytical skill, superior computing power, faster capacity to execute, better (and inside) information, favorable leverage terms, assistance with “techniques” to defer/avoid/evade taxation.

These folks are on the other side of everything I do.

Ruin

Steer clear of most bets where there’s a chance you could lose all your money. Many useful examples in the book.

This doesn’t mean to avoid all loses inside a portfolio. Highly volatile bets can make sense when limited in size.

This does mean avoid creating a portfolio (or lifestyle!) with the potential for total loss.

Kelly Criterion

I do not have faith in my calculations of the probably of real-world outcomes. For me to use Kelly, I need to have a feel for the odds of various outcomes.

Using Kelly weighting (even fractional) runs the risk of fooling myself about the total amount of risk I am taking on. There’s probably a way to work backwards and see the implied odds within various prices – I do not have confidence in my capacity to compete with experts in the arbitrage pricing domain.

That said, the key point I took from the discussion, “never bet an amount that results in a chance, any chance, you’ll be removed from the game.” This calculation is simple to calculate and easy to execute.

Downturns & Drawdowns

With this in mind, there’s an important point about investing for long-term wealth. The likelihood of a major drawdown and the cyclical nature of exponential growth.

Put simply, most families, using a long-term wealth maximizing strategy, will spend a lot of time being “less wealthy than they used to be”. Page 228 of the 1st hardcover edition.

BIG POINT: many families trade a ton of return to avoid this reality // OR // over-bet in the short-term in an effort to avoid normal downward wealth fluctuations.

Worth emphasizing! Most people trade long-term return or increase their risk of ruin to avoid natural fluctuations in wealth (and fitness, for that matter).

Very few people have the emotional make up to roll with the punches when it comes to volatility.

One way to hedge yourself is to maintain the capacity to cut spending so you maintain your “net worth / cash burn” ratio. I write about this a lot because it can give you an emotional edge during a crisis.

Buyer Beware

OK, you say to yourself, I don’t understand how to tail risk hedge so I’m going to use an outside expert to do it for me.

Not so fast!

Focus on your day job. Be really excellent at what you know well. In your financial life, be extremely conservative.

Because…

In every field I’ve gotten to know well…

As a class, insiders consume the excess return for themselves.

I was going to take a break from posting but this topic gives me an opening to share something useful with you.

So here goes.

Sunrises

First, I know next to nothing about crypto.

Fortunately, my life has been set up to take into account that I am clueless about many things!

I think we can start by agreeing that crypto is volatile.

So I’d suggest you start by thinking deeply about how you, your significant other, your family and your coworkers tolerate volatility.

I don’t need to think deeply. My family abhors volatility. They get nervous about stuff we don’t own.

Personally, I tolerate volatility but tend to sell early. By way of example, I am absolutely certain that I would have sold Amazon 20+ years ago. Grateful I didn’t short it.

So, regardless of the fundamentals, I’m not a good fit for the asset.

About those fundamentals, I can’t see them.

I could learn about crypto but, while learning about an asset class that isn’t a good fit, I am not working on something else.

Let’s repeat that… while thinking about one thing, I am not thinking about another thing.

The opportunity cost of mis-directed thought.

Say I get there – I’m comfortable with the asset class, and I’ve gotten myself and my investment committee past the volatility issue.

Will it make a difference?

Buying, not buying, selling, not selling. Being right will not make a difference in my life.

The opportunity cost of incorrect focus. Big one.

Shades of green

If asset classes don’t make a difference then what does?

I was thinking about this on my run this morning. So let’s start with that… dropping fat, maintaining a stable weight, daily movement in nature, improved strength… big difference!

Since shifting my primary focus away from money, my body has had the opportunity to do a lot of cool stuff.

Trying to get more, of what I don’t need, can prevent me from getting something useful.

A flower

Leaving => I wrote about considering if an asset is a good fit for an owner. What about life?

Leaving makes a difference.. every single time I realize I have different values than my peers, I exit => patiently, quietly, doing a good job on the way out.

I need to watch this tendency. Making a habit of leaving is not going to take me where I’d like to go. Stay where I belong.

Building => Don’t look for easy money, build something.

I helped a friend build a business. Unfortunately, he lied to me and stole money from the investors. Interestingly, when the dust settled, that didn’t make a huge difference. If someone isn’t trustworthy then it’s better to know, as soon as possible. In the end, I learned a lot and walked away with 25-years living expenses.

Learning, while building capital => made a difference, up to a point of rapidly diminishing returns.

A reminder of my first kiss with my wife

As you age, I recommend you transition your focus from money to relationships. Because…

Family => marrying well, raising my children to be exceptionally kind and athletic… makes a huge difference, much more than spending the last ten years building wealth would have done.

Having the courage to change, so my kids’ values are a better fit with my own.

My smiling, lovable savages. You have my eyes…

We tend to over-value what we see.

We see crypto rocketing and we think it must be a good idea. It might be. Like I said, I know nothing about it.

But what we don’t see is often more important.

Thinking about that on my run… the decision “to not” has helped in ways I will never see.

Errors not made.

Not smoking, not using scheduled drugs, not taking sleeping pills, not giving into anger, not quitting…

1/. Will this make a difference?

2/. Will “not this” make a difference?

A useful filter on where to focus, and what to avoid.

The tiny dot in the middle of the frame is my son hiking up from a yard sale, in a gale, at the top of Pali Chair. FIVE minutes later he said, “Dad, I’m glad you’re as good a skier as me.” I’d kept my skis during the traverse! They have such short memories.

Our family ski experience is like my Pandemic Predictions => I got a lot wrong.

A friend, with four kids (and a jet), made the observation… “you gotta be able to do something as a family.” Given his role, as the smartest guy I know, we decided to give it a try.

My wife didn’t believe me when I said, in advance, “We’re making a million dollar decision here.”

Frankly, I took it easy on her. The math is daunting…

25 years, $5,000 per annum, 10% p.a. opportunity cost => $490,000

Extend that into your family tree (I have three kids)

Add-in the inflationary effect of surrounding yourself with the largest spenders in our society.

And… have a look around the parking area, with the smell of legal weed wafting across the empty beer cans… Is this an environment where I’d like to leave my teenaged kid unsupervised?

Still… “you gotta be able to do something as a family”.

$175,000 worth of opportunity cost later, I can ski any run, with any member of my family. This makes me happy during a time of year I used to dread.

Total immersion (5 million vertical feet, in three seasons) let me achieve my goal quickly… Something outside, at a high level, with any member of my family.

Unexpectedly worth it… but only after I figured out our family’s cash burn.

I cope with the “demographic” by focusing my energy on seeking to ski like an instructor, with the fitness of a ski patroller. These goals provide structure for my athletic year.

Like much of my outdoor life, my participation is conditional and always one major crash away from ending.

You must be logged in to post a comment.