I had a friend ask me if I thought “cash is king” in the current environment. My answer is more than can fit in a tweet so here you go.

Key Point: when we read reports of monetary policy tightening, I think we are being misled. On a historical basis, policy remains accommodating.

The collective is lousy at remembering history.

US Federal Reserve Total Assets

The value of everything, in the world, has been inflated by the actions of Central Bankers. I think everyone accepts that point. Thing is, it is impossible to measure the scale of the inflation.

In recent memory, the best example will be to cast your mind back to when crypto was a one-way bet.

Asset inflation feeds upon itself, until it doesn’t.

The increase in the size of the Fed’s balance sheet has been a strong tailwind and dominates our collective memory.

If you’re 35 and under, then unprecedented monetary inflation is the only environment you’ve ever known.

Time for another chart.

As at 12 Sept 2022

Here’s a chart of our current reality (black line).

We’ve lived the rate increase, but assets prices have not adjusted to the new reality.

Why?

The economy is rolling along – the tailwind was powerful, and strong

It is unclear where the Fed’s massive balance sheet is going – there has been 13 years of QE – who wants to bet against another round, I don’t

There remains plenty of OPM (other people’s money) and leverage

Those are equity, bond and money market funds I track, as at last Monday.

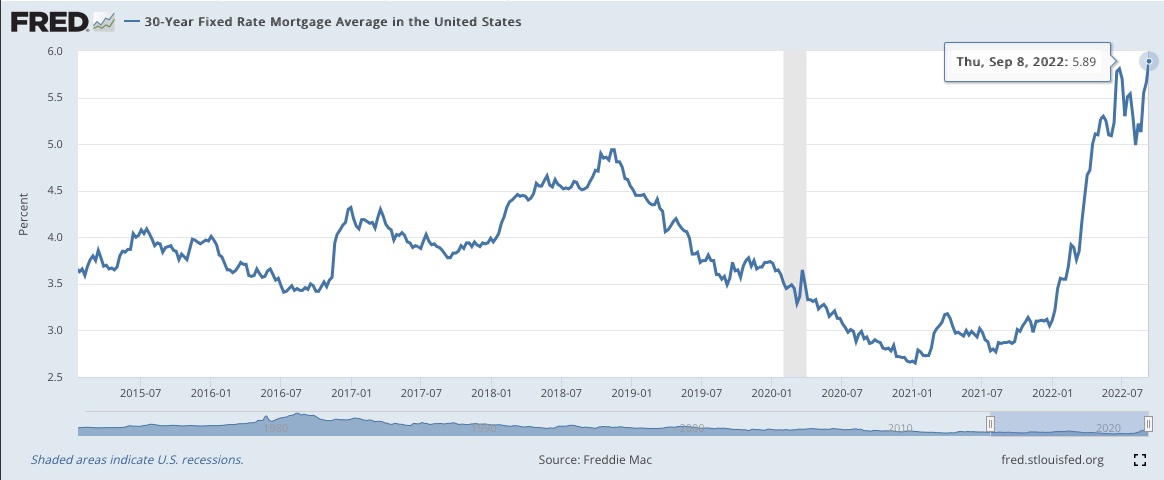

US 30-year Mortgage Rates 2015-now

Mortgage rates appear to have jumped.

However, let’s have a look at the next chart.

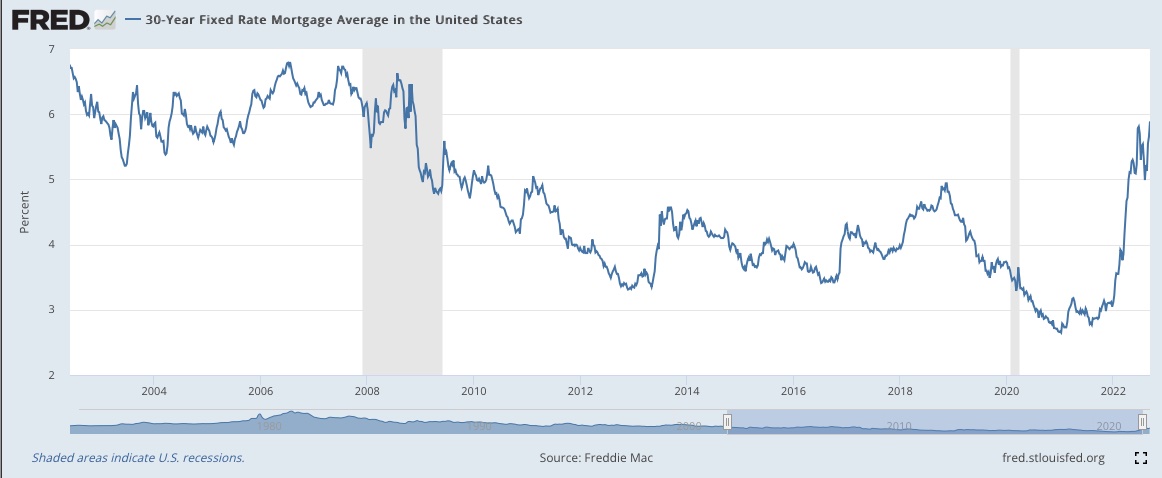

2003-now

Rates are only just getting back to their 2003-2008 level, a time when people were hardly holding back on real estate.

So what do I think:

1// Assets could get cheaper – I don’t see any case for a melt up.

2// If the Fed materially shrinks their balance sheet then assets will get a lot cheaper. Cutting their balance sheet in half takes us back to 2015.

3// Sit down and ask yourself “what if” asset prices drop to 2015 levels, a 50% reduction. Odds are, you have your interest rates locked in. So the main risk will be short term cash flow due to unemployment. How might you protect yourself?

4// Having a year’s core cost of living in an “emergency” fund makes sense. Personally, I didn’t reinvest the proceeds from a Q2 asset sale. My reserve is enough to navigate a nasty recession without selling anything further.

So a “prudent cash reserve” is King.

I don’t think it makes sense to liquidate positions, and pay extra taxes, because risk assets might fall in value.

It’s been 60 days and we’re starting to see the beginning of the adjustment from higher rates. Average 30-year mortgage chart below.

Looking back One Year

Inventory is back at pre-COVID levels and prices are moving sideways. My feeling is the market is going to get cheaper.

This is a yield-based feeling.

Let’s look at the current yield curve.

Black 2022 vs Blue 2021

A simple metric I use for vacation markets.

What is “one week rental” relative to capital value?

I priced two markets this past week. These are not Christmas or Holiday Weekend rates, but they are December to February high season weeks.

Jackson – $10,000 a week relative to $4-6 million capital value

Vail – $5,000 a week relative to $2-4 million capital value

This is where the Yield Curve is useful – the 6 mth (to 30-year) rate is ~3%

3% of $5 million is $150,000 per annum vs $10K a week to rent

For nearly all users, the secondary market has swung strongly in favor of rent vs buy.

Other impacts… the stock market ~19% off its peak, crypto down, commodities down, China property market under stress, hot war in Europe, US Fed in a tightening cycle…

These changes, combined, are making marginal buyers less wealthy.

All prices move at the margin.

What does this mean?

My #1 investment principle is to construct a life where I don’t need to be right.

If the Central Banks are done bailing out financial assets then it makes sense for the price of financial assets to fall. The free-money era pulled returns forward and some of that will need to go back into the future.

That said, the recent past shows a clear bias towards continuous financial bail outs.

Impossible to know what will happen.

A note on inflation, as I see it.

If you own financial assets then you’ve been “paid” in asset appreciation over the last few years – SP500 is up ~50% over last 5 years.

Going back further, say 2010, the owners of financial assets have grown accustomed to unearned wealth.

So the best hedge against the market (& inflation) was letting personal spending decline, as a percentage of family assets, across the run up.

If you didn’t own assets then, hopefully, you’re in a skilled profession where you’ve been able to increase your income faster than inflation. If not then your best investment is up-skilling yourself.

The recent past, and media, are skewing your perception of inflation.

What’s your best guess for the 10-year breakeven inflation rate?

It peaked at 3% in the spring, currently 2.4%

1.03 ^ 10 = 1.34, 34% price increase over last 10 years

If, like me, you were building a family then your core cost of living is up WAY more than 34%.

When I look at our family budget, I can see a big part of our increase is lifestyle inflation.

For many of us: the long bull market has driven lifestyle inflation well ahead of the price inflation we’ve experienced.

Again, the best hedge is either: (a) not ramping spending, or (b) staying variable so the family can cut spending quickly, if required.

For perspective compare 34% 10-year inflation to…

SP500 10-year total return => 175% increase

The 10-year price of wherever you happen to be living

Short-term price inflation is nothing compared to long-term asset value inflation.

Given the future is unknowable (bailouts, ZIRP and money creation):

The most “costly” part of the pie is whatever you happen to believe is “essential.” It usually doesn’t feel this way => you truly believe you need this stuff. I feel the same!

When you suffer your first serious setback, you’ll be surprised how little is essential. In 2009, I cut my “essential” in half, overnight.

Similarly, as we age, we may find we were giving time, money and attention to things that don’t seem to matter anymore.

Know your buckets – they will help you think more clearly.

Specifically, Net Worth expressed in “years spending.”

$1,000,000 / $125,000 = 8 years

As we change the spending, we change the years.

Risk, and INFLATION, are easily mitigated when you understand how easily you can change spending.

Risk Concept => not all spending, or financial obligations, are created equal

Be most aware of:

Debt, including contingent – an obligation where non-payment can force the sale of an asset

Spending that comes with spending – large HOA/Club fees come to mind here – put plainly, a hotel visits feel just the same on an ego, yet, don’t require an annual membership fee

Going further => Don’t Capitalize Luxury Spending => the “luxury bucket” from above, if you turn it into a capital obligation then it can bite you, especially when combined with debt.

We don’t need to own the hotel to receive the services offered to a guest.

Same with… plane, waterfront, ski chalet… whatever you find inside your “luxury” bucket.

Staying flexible with the ability to stop spending can feel like a “waste” – even more so when highly-leveraged peers appear to be making easy money.

This feeling is false!

We over-estimate the value of current spending

We adapt very quickly to any level of spending

We notice changes, not absolutes

You are paying for the flexibility to: (a) stop paying; (b) change your mind; and (c) keep your capital invested productively.

The realization I was spending on things that didn’t make me happy drove positive changes in my life.

In Private Equity, I was surrounded by rich people who struggled to apply their financial wealth towards improving their lives.

My climb up the ladder saw me scale consumption and reinforce my ego.

Until one evening, recently divorced, sitting alone in a fancy townhouse…

I realized the only thing left inside my current path was “more money”

What To Do?

++

Consider Declaring Victory

More money will not be making your life any better. In fact, you’re now in danger of being able to ramp consumption in a way that makes your life more complicated.

If you don’t believe me then think about your most recent financial loss. The loss hurts, it’s a distraction, you find yourself wanting more and more…

…but you already have more than your younger self thought they needed?

To think clearly, you need to get out of your environment.

In the summer of 2000, I took a two month leave of absence and trained for triathlon in the hills above Boulder, Colorado.

I journaled, while training to quality for Ironman Hawaii.

Got a bucket list? Go do something on it. Do another. And another.

In my case, I kept on the same thing=> faster, and faster, and faster…

++

WHILE LIVING THE DREAM…

Do You Have A Committed Long-Term Relationship?

I didn’t. You might.

This person is your most valuable asset.

Live your dream WITH THEM.

High achievers, quite often, are short-sighted about the value of relationships vs completing “the mission.”

++

Don’t have a relationship?

Consider moving to a location where there are a lot of people who share your values & culture.

Once there, focus on making YOURSELF into the person you’d like to attract. It’s took me five years to meet my wife, be patient.

My values:

an active outdoor life

surrounded by nature

athletic

kind & reliable

Yours?

Write it down.

++

Do You Have Kids?

Your future self would like you to get to know them, very well.

Why?

If you blow off (the difficulty of toddlers) then you’ll end up with a regret you can’t fix!

You don’t need to become a preschool teacher.

When they were little, I could only handle a few hours a day with my crew…

…but they were very useful hours.

I was able to train my kids to become my partners in exploring the world. I trained our little ones during 1-on-1 trips. They have a lot of very happy memories.

There has been a HUGE payoff. From the time they were 7 years old, my kids have been able to do really cool stuff with me.

Know your best environment – teach them there – 1-on-1

Remember this => don’t let your adult agenda derail the child’s joy in simply being there.

Fill your child with pleasant memories of doing stuff with you.

G – Literally Just listened to your catalyst podcast – excellent!!!! Wow, truly good – thank you for putting that out there. I took 8 pages of notes and I have already read your writing for decades

You must be logged in to post a comment.