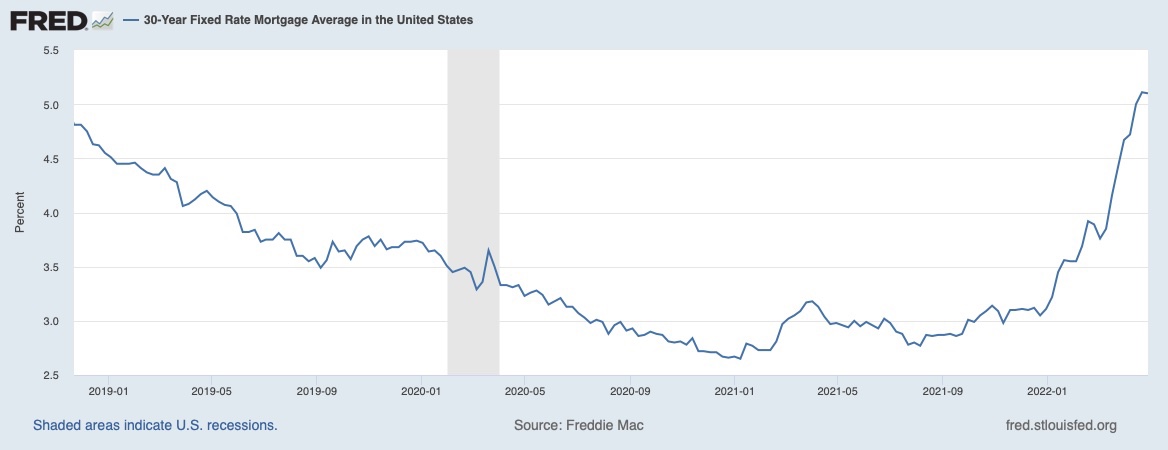

It’s been 60 days and we’re starting to see the beginning of the adjustment from higher rates. Average 30-year mortgage chart below.

Looking back One Year

Inventory is back at pre-COVID levels and prices are moving sideways. My feeling is the market is going to get cheaper.

This is a yield-based feeling.

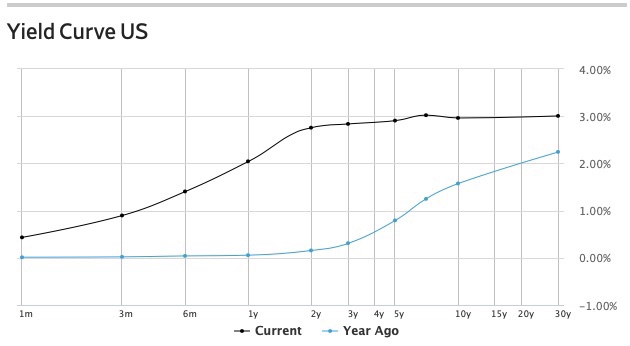

Let’s look at the current yield curve.

Black 2022 vs Blue 2021

A simple metric I use for vacation markets.

What is “one week rental” relative to capital value?

I priced two markets this past week. These are not Christmas or Holiday Weekend rates, but they are December to February high season weeks.

Jackson – $10,000 a week relative to $4-6 million capital value

Vail – $5,000 a week relative to $2-4 million capital value

This is where the Yield Curve is useful – the 6 mth (to 30-year) rate is ~3%

3% of $5 million is $150,000 per annum vs $10K a week to rent

For nearly all users, the secondary market has swung strongly in favor of rent vs buy.

Other impacts… the stock market ~19% off its peak, crypto down, commodities down, China property market under stress, hot war in Europe, US Fed in a tightening cycle…

These changes, combined, are making marginal buyers less wealthy.

All prices move at the margin.

What does this mean?

My #1 investment principle is to construct a life where I don’t need to be right.

If the Central Banks are done bailing out financial assets then it makes sense for the price of financial assets to fall. The free-money era pulled returns forward and some of that will need to go back into the future.

That said, the recent past shows a clear bias towards continuous financial bail outs.

Impossible to know what will happen.

A note on inflation, as I see it.

If you own financial assets then you’ve been “paid” in asset appreciation over the last few years – SP500 is up ~50% over last 5 years.

Going back further, say 2010, the owners of financial assets have grown accustomed to unearned wealth.

So the best hedge against the market (& inflation) was letting personal spending decline, as a percentage of family assets, across the run up.

If you didn’t own assets then, hopefully, you’re in a skilled profession where you’ve been able to increase your income faster than inflation. If not then your best investment is up-skilling yourself.

The recent past, and media, are skewing your perception of inflation.

What’s your best guess for the 10-year breakeven inflation rate?

It peaked at 3% in the spring, currently 2.4%

1.03 ^ 10 = 1.34, 34% price increase over last 10 years

If, like me, you were building a family then your core cost of living is up WAY more than 34%.

When I look at our family budget, I can see a big part of our increase is lifestyle inflation.

For many of us: the long bull market has driven lifestyle inflation well ahead of the price inflation we’ve experienced.

Again, the best hedge is either: (a) not ramping spending, or (b) staying variable so the family can cut spending quickly, if required.

For perspective compare 34% 10-year inflation to…

SP500 10-year total return => 175% increase

The 10-year price of wherever you happen to be living

Short-term price inflation is nothing compared to long-term asset value inflation.

Given the future is unknowable (bailouts, ZIRP and money creation):

Do you ever feel you are behind? That you don’t have enough? That you might run out?

What to do?

Make vague feelings real by writing down some specifics.

Then get to work.

ONE => Is this a Reference Set issue?

If I spend time in Aspen then my “needs” escalate, and my self-assessment “declines.”

Same deal in Boulder, but it’s from a fitness point of view.

Others might have vanity triggers in places like LA, or on Instagram!

Feelings are sensitive to environment. The same life, done somewhere else, will be different.

Feelings of envy, fear and anxiety are sensitive to images – careful with environment, turn off cable news, get off Facebook/Instagram.

++

TWO => Is this a Skills issue?

A 35 yo surgeon with $250,000 of education debt, is in a different position than most. The surgeon is likely to earn themselves into financial security.

Where does my current job track lead?

Do I need retraining?

Armed with additional skills, it is easier to move up the income ladder?

Do I need to do the same job for a higher bidder?

What is the market rate for my skill set?

++

THREE => Is this a Spending issue?

It’s not always spending… but sometimes it is, particularly when spending isn’t generating satisfaction.

If you have the skills & the salary, but are left feeling uneasy, then a family financial review can make sense.

These discussions are HIGHLY emotional. I recommend a skilled facilitator.

++

FOUR => Is this a Time Horizon issue?

Back to the surgeon… highly skilled, employed, spending under control… the situation is going to play out just fine.

Pay down debt

Keep spending in check

Conservative monthly investment program

15 years along, the family is in a strong position. They had doubts, I did not.

I was asked, what would I have done?

Starting over at 40 yo

Core Job matches my highest paying skill set. Medicine, tech, finance, aviation… track into something that pays well.

The Core Job enables me to borrow long for a Core Investment. Buy real estate in a zip code with great public schools and a diverse local economy.

Secondary Job in an area of personal interest. It’s what many do with coaching/consulting.

Side Projects with Equity Upside. I would be looking for opportunities to invest (primarily time) in situations with financial upside. Do enough of these and something is likely to hit.

One new skill each year – coding, online marketing, blogging, video content, copywriting, language, ministry, education, graphic design, photography… stacked across a decade… powerful.

Core Job

Secondary Job

Equity Upside

Continuous Learning and Skill Acquisition

I have a friend, who did all of the above.

Around 40 yo, they were divorced

Then their employer went bust

Then they found our their pension had invested in the employer

So the pension went bust…

Long story short, a rapid journey from “set” to “f*%^ed”.

They could see “effective net worth” was negative due to financial obligations related to the divorce.

What I saw for a decade…

Three jobs: two of the jobs had flexible scheduling. Time off was used to work continuously (7/52/365). The third job was consulting, which was done inside the daily gaps.

Modest spending: given the income rolling in, not much went out.

Heavy investment: every single month, buy financial assets. Take overtime, buy more. Bonuses and financial windfalls, buy more. Buy, buy, buy.

This path isn’t for everyone – it comes with a cost in terms of family life. You need a spouse, who is completely on board. It’s a team effort.

A decade of grinding and the family is in a strong position. Now, the challenge may be to shift away from financial assets and build multigenerational Human Capital.

Final Word

Think deeply about Reference Set

There is a weak link between financial assets and life satisfaction

We never get time back

Too often wants are driven by external influences

Know what feeds your soul – write it down, take your shot

Make the target clear to yourself – for me => an active, outdoor life sharing experiences with friends and family

In March 2020 I increased equity allocations to 72% of my Vanguard portfolio.

Allocating additional capital in 2022, I made a reserve for “an investment that benefits the present”…

…then rebalanced to 60% equity allocation.

This reduced the size of the new investment and got me past decision paralysis, driven by a fear of near-term loss.

The reserve now sits at ~15 years Core Cost of Living.

Looking pro

We’ve been looking around for a place in the mountains.

Coming off a year of AirBnB skiing, I know our cost to rent implies a gross yield of 0.75 – 1.75%.

Alternatives to buying:

Stick the Strategic Reserve into VTSAX, rent through AirBnB and let dividend growth hedge rental inflation

Stick the Strategic Reserve into a medium term bond product (VBTLX @ 3%) and earn a margin over my cost to rent

Pursue either of the above, double my discretionary spending and run the capital down between now and my wife’s 85th birthday

For now, I’m taking Door #4

Rebalance after large (down) moves

Watch the Federal Reserve increase rates

See what happens

A 35% market decline implies a dividend yield over 2.25%, which would let me lock in the equivalent of three-months cost of living (after tax, forever).

I tossed my idea of buying a Sprinter Van for camping. The shift towards “assets for fun” doesn’t come naturally.

At the closing, my agent (50-ish) shared that the only recession he’d really experienced was 2008/2009. So the next chart is his personal experience with asset pricing.

Right hand corner blip looks a little bigger

The above chart is ~20-years of mortgage rate history. If you’re 40-something this is what you lived.

At 53, my life is changing. The window of what I need to finance is less and less. I have begun a strategic shift towards creating the life I want to live in my 60s.

Real Estate is lumpy, we don’t have the ability to incrementally rebalance. I wanted to reduce exposure before making any additional purchases.

The sale was valued at 43 years gross rental income (2.3%). Cash proceeds, after tax, were 64 years net rental income (1.6%).

Institutional Memory is 1,000 days, max. Here’s the last 1,000 days in the mortgage market.

The real estate market is like a super tanker, it takes a long time for momentum to shift. After the 2008/2009 recession, non-foreclosure prices didn’t adjust until the middle of 2010.

Prices move at the margin => the marginal buyer had a strong tailwind through the pandemic, that has changed in 2022.

There will be an impact of the near-vertical move in rates this year => initially, we will see this in markets that require loans to complete.

The scale of “the impact” is unknowable and complicated by supply shortages of re-sale houses and for new build.

Prices are being supported by rapidly rising cost-to-build and cost to renovate/remodel.

Lots going on – I can make a case for +25% and -25%.

At 53, taking 64 years-equivalent cash-flow off the table, in a rising rate environment, is a decision I’ll be able to live with regardless of future outcome.

Teach your kids their financial lives will be about no more than a dozen choices.

Here are mine:

Study finance (class of 1990)

Save 50% of my take home (1990-2007)

Partners investment scheme (late 90s, all in then, equivalent of 1 yr spending now)

Work to build a startup (2000)

Sell into the frenzy (2005-2007)

Move into a low-cost Vanguard portfolio (2008 onwards)

Boulder real estate (2010 & 2012))

Downsize (2012-2013)

Borrow long at 3.25% (2013)

Debt free (2007 & 2020)

Have kids with a kind woman from a humble background (on going)

Every other choice turned out to be noise. What to do?

Focus on actions, not outcome.

What does that really mean?

Do what moves you forward and have faith. Sport, marriage, money, all things… daily action is the fundamental force moving you towards “better.”

Education matters => I was given a chance in Private Equity because I had high marks in a useful field. Between my high school graduation (1986) and my youngest’s (2031) the nature of “useful” will have changed. However, the need for skilled people to “do” will endure.

The most useful part of my degree wasn’t finance! It was financial accounting, programming and mathematics => I learned fundamental knowledge in college. I learned my profession on-the-job. You learn the valuable part by doing work, for the best people you can find.

This keeps popping up over and over again (professors, partners, coaches, mentors, twitter follows). At 53, I’m learning from people less than half my age! Do work to learn.

Avoid Ruin => studying, then working in, financial accounting helps you learn when a situation doesn’t feel right. Embezzlement is an old game and it’s useful to learn the patterns. Financial fraud happens, and will continue to happen. Take steps to reduce your family’s exposure to ruin.

With the accounting, I learned the most with 9 credits spread across three courses. Financial Accounting 1, 2 and 3. Small investment, huge return. Do it when you’re young. Being forced to rely on others to do your financial math is a disadvantage that will cost you.

Let’s pull it together for you…

Starting your working life (in a useful field, with your financial accounting courses done)…

Waiting for the fat pitch – once in a lifetime investment opportunities happen once a decade

Turning yourself into the sort of person you’d like to marry, the friend you’d like to have, the parent you aspire to be => meaningful connection is true wealth

Your mind will try to trick you into thinking it’s the investment choices that matter.

It is not.

It is the four habits I outlined above, and avoiding substance abuse.

My kids won’t fully appreciate my choices until after I’m gone.

My #1 financial goal for my kids is debt-free education in a field that enables them to get paid.

With the very best of intentions, the US Government has completely screwed up both (a) the cost of college education and (b) the financial lives of the students they were seeking to help.

Debt isn’t free.

Every market juiced with easy money gets screwed up.

Explanation below – my life mirrors the blue line – graduate early, debt free, start saving

I googled up average debt at graduation and average graduation age.

$40,000 and 23 yo.

So let’s make three simple scenarios:

Debt free early graduation (21 yo) => McGill 1990 finance grad

Debt free at 25 yo

Debt free at 30 yo

Let’s run it forward assuming:

Investment return of 5%, prior year close

$20,000 per annum savings

The late-start saver

who saves at the same annual rate

who earns the same return

ends up ~$1 million behind at 60 yo.

This is not the whole story, not even close!

In my demographic, families can burn ~$250,000 of capital to help a kid “get started” => 529 accounts and parental support. Even more if you roll private from Kindergarten.

What’s the 30-year cost of this choice?

$250,000 * (1.05)^30 = $1,080,000

Million bucks gone, you never see it.

You burned the capital

The kid figures life out by 30, and spends most of their 20s pissed at you (for tapering their support) 😉

$2 million opportunity cost, spread between two generations.

You assume it was what you were supposed to do and are grateful you finally got them off the payroll.

A possible alternative…

Our default position is in-state education and I’ll buy whatever’s left of your 529, at $2 on the dollar, once you save $100,000 of your own money.

That article introduced the concept of Lifestyle Sustainable => a low-cost base of operations where, ideally, you can live for free. The idea is to remove cost-of-housing from your financial concerns.

That’s the core financial asset for your portfolio. It cost me US$110,000 in 2000.

This is a great place to park your Core Capital.

Removing housing from your list of concerns gives you more than a financial return.

Alongside your key financial asset, I hope you have a loving, lifelong partner. This person is the most important decision, financial or otherwise, you’ll be making.

The highest return investments I made in my 30s & 40s, were not financial in nature. With a low-cost base of operations, & marketable skills, I was in a good place.

Many high-earners fail to see the value of what I just pointed out.

Low-cost base of operations

Marketable skills

Beyond that, most everything is lifestyle enhancement and ego.

Thankfully, I had a major setback in my early-30s (divorce) which gave me pause.

In 2000, I saw my future in front of me… lifestyle enhancement and ego… and I made a change.

A big one.

I became a world-class athlete. With (athletic) success came the realization that something was lacking.

So much success, still lacking!

If you’re good at making money…

If you’re good at playing the game of “career”…

If you are nearing the top of your field…

…then you’ll be tempted to keep doing what you are good at.

I’d encourage you to establish that low-cost base of operations, then try something really challenging…

The highest return investments I made were improving my suitability for marriage and learning how to parent. Most of my learning happened after I was married and my kids were born.

It is never too late to invest in the human capital of your family.

If you get these investments right then you might not notice the benefits. Honestly, a big driver in my life has been a fear of getting divorced again (not-divorced, winning)

Fear that drives positive action is useful.

I’ve been paid by less drama, and less problems (we don’t see all our wins).

I’ve also de-risked some of the challenges my future self will face (companionship, engagement, dementia). Study (the problems of) who you are likely to become.

You’ll notice my portfolio advice (still) doesn’t talk about asset allocation.

This is deliberate!

Asset selection is not the differentiating factor for a life well lived.

Marketable skills

Low-cost base of operations

Fixed-rate mortgage, if you like

Target date fund for your future self

Then focus on living your life and creating the friends/family with whom you’d like to share it.

You must be logged in to post a comment.