In March 2020 I increased equity allocations to 72% of my Vanguard portfolio.

Allocating additional capital in 2022, I made a reserve for “an investment that benefits the present”…

…then rebalanced to 60% equity allocation.

This reduced the size of the new investment and got me past decision paralysis, driven by a fear of near-term loss.

The reserve now sits at ~15 years Core Cost of Living.

Looking pro

We’ve been looking around for a place in the mountains.

Coming off a year of AirBnB skiing, I know our cost to rent implies a gross yield of 0.75 – 1.75%.

Alternatives to buying:

Stick the Strategic Reserve into VTSAX, rent through AirBnB and let dividend growth hedge rental inflation

Stick the Strategic Reserve into a medium term bond product (VBTLX @ 3%) and earn a margin over my cost to rent

Pursue either of the above, double my discretionary spending and run the capital down between now and my wife’s 85th birthday

For now, I’m taking Door #4

Rebalance after large (down) moves

Watch the Federal Reserve increase rates

See what happens

A 35% market decline implies a dividend yield over 2.25%, which would let me lock in the equivalent of three-months cost of living (after tax, forever).

I tossed my idea of buying a Sprinter Van for camping. The shift towards “assets for fun” doesn’t come naturally.

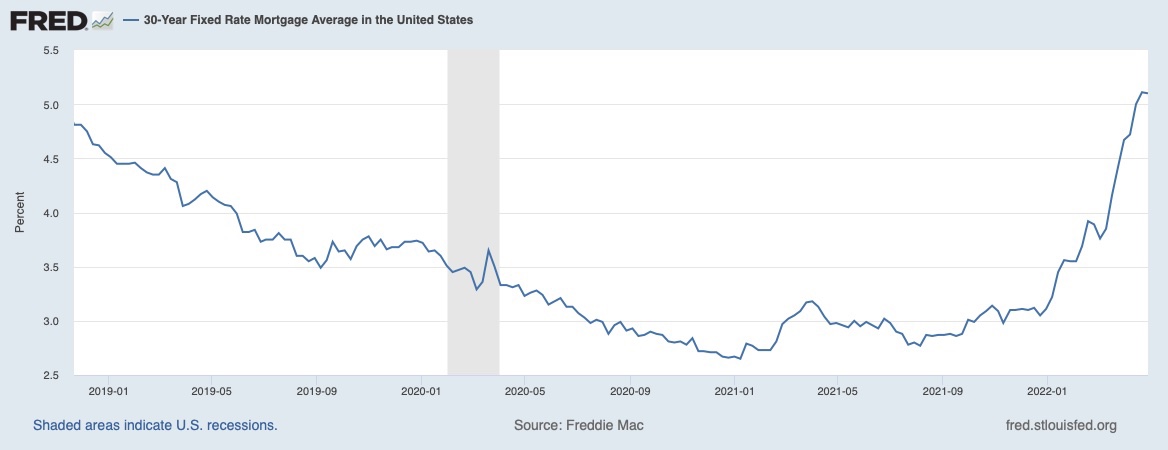

At the closing, my agent (50-ish) shared that the only recession he’d really experienced was 2008/2009. So the next chart is his personal experience with asset pricing.

Right hand corner blip looks a little bigger

The above chart is ~20-years of mortgage rate history. If you’re 40-something this is what you lived.

At 53, my life is changing. The window of what I need to finance is less and less. I have begun a strategic shift towards creating the life I want to live in my 60s.

Real Estate is lumpy, we don’t have the ability to incrementally rebalance. I wanted to reduce exposure before making any additional purchases.

The sale was valued at 43 years gross rental income (2.3%). Cash proceeds, after tax, were 64 years net rental income (1.6%).

Institutional Memory is 1,000 days, max. Here’s the last 1,000 days in the mortgage market.

The real estate market is like a super tanker, it takes a long time for momentum to shift. After the 2008/2009 recession, non-foreclosure prices didn’t adjust until the middle of 2010.

Prices move at the margin => the marginal buyer had a strong tailwind through the pandemic, that has changed in 2022.

There will be an impact of the near-vertical move in rates this year => initially, we will see this in markets that require loans to complete.

The scale of “the impact” is unknowable and complicated by supply shortages of re-sale houses and for new build.

Prices are being supported by rapidly rising cost-to-build and cost to renovate/remodel.

Lots going on – I can make a case for +25% and -25%.

At 53, taking 64 years-equivalent cash-flow off the table, in a rising rate environment, is a decision I’ll be able to live with regardless of future outcome.

G – Literally Just listened to your catalyst podcast – excellent!!!! Wow, truly good – thank you for putting that out there. I took 8 pages of notes and I have already read your writing for decades

That article introduced the concept of Lifestyle Sustainable => a low-cost base of operations where, ideally, you can live for free. The idea is to remove cost-of-housing from your financial concerns.

That’s the core financial asset for your portfolio. It cost me US$110,000 in 2000.

This is a great place to park your Core Capital.

Removing housing from your list of concerns gives you more than a financial return.

Alongside your key financial asset, I hope you have a loving, lifelong partner. This person is the most important decision, financial or otherwise, you’ll be making.

The highest return investments I made in my 30s & 40s, were not financial in nature. With a low-cost base of operations, & marketable skills, I was in a good place.

Many high-earners fail to see the value of what I just pointed out.

Low-cost base of operations

Marketable skills

Beyond that, most everything is lifestyle enhancement and ego.

Thankfully, I had a major setback in my early-30s (divorce) which gave me pause.

In 2000, I saw my future in front of me… lifestyle enhancement and ego… and I made a change.

A big one.

I became a world-class athlete. With (athletic) success came the realization that something was lacking.

So much success, still lacking!

If you’re good at making money…

If you’re good at playing the game of “career”…

If you are nearing the top of your field…

…then you’ll be tempted to keep doing what you are good at.

I’d encourage you to establish that low-cost base of operations, then try something really challenging…

The highest return investments I made were improving my suitability for marriage and learning how to parent. Most of my learning happened after I was married and my kids were born.

It is never too late to invest in the human capital of your family.

If you get these investments right then you might not notice the benefits. Honestly, a big driver in my life has been a fear of getting divorced again (not-divorced, winning)

Fear that drives positive action is useful.

I’ve been paid by less drama, and less problems (we don’t see all our wins).

I’ve also de-risked some of the challenges my future self will face (companionship, engagement, dementia). Study (the problems of) who you are likely to become.

You’ll notice my portfolio advice (still) doesn’t talk about asset allocation.

This is deliberate!

Asset selection is not the differentiating factor for a life well lived.

Marketable skills

Low-cost base of operations

Fixed-rate mortgage, if you like

Target date fund for your future self

Then focus on living your life and creating the friends/family with whom you’d like to share it.

We are living through boom times in our local real estate market. Houses are selling quickly, at the equivalent of 50-100x annual rent.

Everything, other than debt pricing, looks expensive to me. So… I’m looking to move, borrow and increase the assets in my portfolio that generate cash flow.

A simple way to view this… (a) split the equity in your existing house in two parts; (b) borrow 30-year fixed and buy a new place with one part of the equity; and (c) place the other part into a rental property.

The explanation follows, with a 25-year overview at the end.

In 2010, I purchased two rental properties as a hedge. Specifically, I wanted to hedge against the risk of my family being priced out of our home market. I thought I was protecting my kids. Turns out I was protecting myself.

The idea was to get paid (via rental income) to hold: 3 units, 10 bedrooms and 20,000 sf of Boulder land. The locations were excellent, the properties dated.

The 2010 purchases worked out well, not just because they performed. The purchases put significant cash pressure on me. The pressure improved my spending choices and motivated me to sort a business which was hemorrhaging cash. In a sense, having tight cash was a form of forced savings.

In 2013, we downsized, borrowed and moved across town. By staying in the same type of neighborhood, and borrowing modestly, our equity appreciation in the smaller house ended up the same as what we would have earned in the larger, unleveraged house.

My ego likes headline numbers and struggles to accept this reality. Something about real estate => the gross, headline numbers are more emotionally salient than the net cash flow reality.

Once again, I’d like to free up time, and reduce admin, by moving. The price I’m going to pay is time/hassle from the move, bringing some deferred taxes forward and agent’s fees.

With the run up in asset values (2015-2021), my family has a much larger allocation to “dead assets.” Dead assets are assets that cost money to hold => for many readers, this is the house they live in. Given recent capital appreciation, the cash cost to hold has been ignored by many.

Downsizing, and locking in 30-year fixed debt for a portion of the new purchase, enables me to keep the amount of “dead assets” modest within the family portfolio.

My ego is tempted to size up, and add a ski place. The better financial move is to improve the quality of our rental portfolio, while reducing my housework and driving.

30-year fixed debt on the family home is one of the best deals going. Given the borrower’s option to repay, it’s a one-way option that could be worth big $$$ in the future.

A word to the leveraged.

Now, like 2005-2007, is a great time to be heavily indebted. You will take comfort in your ability to unwind any financial difficulties.

You are correct.

However, if you truly “need” to unwind financial positions then we are likely in a market like 2009, unpleasant.

So be cautious with opting-in to risks that don’t add to your long-term strategy. Most particularly, any arrangement where an outside party has the power to force a sale. While I am seeking to borrow, total debt will remain modest relative to assets and cash flow.

Breaking it down, building wealth across decades.

Resist the urge to up-size your life, particularly by adding negative yielding assets.

Rather, seek to build up 2-4 rental units. Pay attention to location, lot size and bedrooms.

Unless you want to get into the hotel management business, rent unfurnished to long term tenants. Inverting I have learned… furnished, short-term rentals bleed expenses, emotion and time.

For your long-term rentals, use a local property manager – their cost as a %age of capital value will be tiny compared to the value they add, and the hassle you avoid. This frees time to make money in a field where you have an edge => whatever you were doing when you built up the $$$ to purchase rental properties. Side Note on taxes: tax bill as a %age of net assets is a number you should track.

Use your personal home for shelter, as an entry in the best public schools in your state, as a cheap source of fixed rate debt and a tax-favored investment. If this asset appreciates to the point where you have “too much” invested in non-yielding real estate then downsize, get a new mortgage and repeat the cycle.

Aside from the roof and HVAC… spend no material capital on any of your properties. Instead, spend time with the people you love (and buy more assets that generate cash flow).

If you start the above when you get married then you’ll have 1-3 moves by the time you are empty nesters. At that point, you’ll have built yourself an inflation-proof, tax-effective retirement annuity. You can constrain your spending and pass it to your grown kids OR run down the assets as you see fit.

That’s the financial overlay. You also have the ability to use trust structures within this strategy. I’ll get to those in a future post. Put simply, when I say “you” it’s possible to put a trust in “your” place. That can protect your assets from the unexpected which, over a 25 year time horizon, is nearly certain to happen.

Ideally, you graduated debt-free from college and made a habit of maximizing your retirement contributions in the first 10 years of your career. Don’t be in a rush to get into real estate, I’d been working/saving for a decade before I had the capital, and geographic stability, for a purchase to make sense. While a favorite form of security for lenders, real estate is chunky, a pain to manage and expensive to sell.

A good question to consider with major assets in a portfolio…

Would I buy at current prices?

Like most real estate in Colorado, Boulder capital values have been on a 7-year upswing. According to Zillow, the capital value of where we live is $2.5 million, up 36% since the start of 2020. The only way to describe how this value feels is “too high”.

One way to consider capital values is to express them in terms of cash flow and time => with real estate, the proxy is cost to rent.

With our current address, comparing rental costs with gross capital value…

$3,000 per month rental => 69 years equivalent

$4,500 per month rental => 46 years equivalent

$6,000 per month rental => 35 years equivalent

With the run-up in prices, homeowners have been rewarded for properties that are larger than their needs. Like-for-like rental, doesn’t look too crazy right now. However, we could easily fit ourselves into a location that’s 40% smaller than where we live at present (implying a gross yield of less than 2%).

On to the next example…

++

In 2021, some friends exited the Boulder real estate market. Their net sales proceeds (after taxes and agent’s fees) equate to ~100x their first year rent in their new location.

Worth repeating: they are taking a century of rental-equivalent off the table.

Put another way: by selling into this market they can do the following (in current dollars):

Cover their future cost of living on a joint-life expected basis;

Put their kids through college;

Buy an apartment as a hedge against future rental rates; and

Treat future earned income as fully discretionary.

Compelling, especially if your house is the primary asset in your balance sheet.

They aren’t “set” by any means: inflation, illness, increased spending or investment losses might derail their plan. However, the asset sale greatly reduces their financial stress and buys them a tremendous amount of time.

Stress, time and the risk of ruin.

++

Another example, vacation properties.

The house we rented in Vail (2019/2020) is valued at more than 100x the rental we paid. The condo we rented in 2018/2019 sold for 50x annual rental.

There’s never been a better time to rent assets you don’t need. 😉

If you own assets in secondary locations, or are considering buying, then the above calculation is a useful one to consider. The numbers above are using gross rental figures. From the landlord’s point of view, the net rental income would be tiny (relative to capital).

Also consider the benefits of being variable…

Rather than lock in a single location for the winter, I’ve decided to try an AirBnB season. I booked in 22 days of skiing, the dates tie to school holidays => Vail, Telluride and Jackson.

Adding a bit of airfare, gas and mileage… total cost will be $15,000 to use properties with an average value of ~$1 million. VTSAX dividend yield is 1.25%.

By not owning, it was cost-free to change strategy.

++

Other questions I like to ask:

Assume things go well and this asset doubles in price (again), who’s going to buy?

What’s going to drive the next doubling in value?

Where’s my family exposure: (a) benefiting from the next doubling; or (b) harm from the risk of a halving?

Who’s going to buy? A smaller place in a great neighborhood is much easier to sell than the best place in that neighborhood. The top places in Boulder are now selling for around $5 million. Who’s going to buy when the market goes to $10 million? Might “ability to purchase” create headwinds for appreciation in the market?

Prime Colorado real estate benefits from buyers coming from “even more expensive” markets. Boulder remains a great place to land from one of our coastal Metros. City-based housing markets benefit from local economic growth.

Vacation-markets, at 50-100x gross rental income, are reliant on continued balance sheet appreciation for the Top 1% of society.

A comparison I follow in Colorado… Boulder rental property (house with land, no HOA) vs Vail vacation property (condo w/o land rights, HOA). In the last recession, I tracked this comparison in Arizona – unfortunately, I bought condos down there instead of houses.

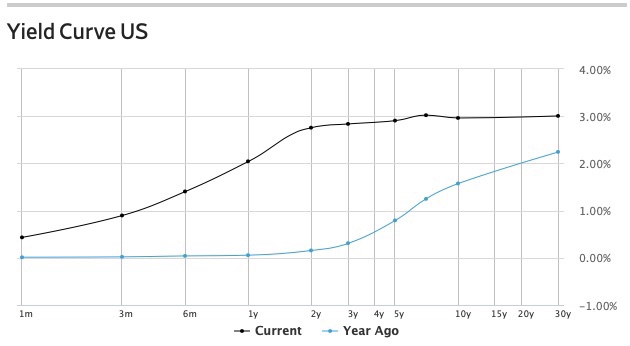

What’s going to drive the next doubling? See the chart at the top of this post => there’s been a multigenerational tailwind due to declining interest rates. Every store I enter, and every manager I talk to, gives multiple examples of tight labor & inflationary pressures.

Negative real interest rates might keep the party going for a bit. With Social Security COLA adjustments over 5%, it seems nuts to buy into property that’s trading on 50-100x rental income.

Family exposure. For me this is kind of like the “who’s buying” question.

If you’re a double-income family with a diversified portfolio then sticking 10-15% of assets into a vacation market is a different choice than a single-income family with 90%+ of assets tied up in a mortgaged home. The context of the choice is worth considering.

One final point, despite living at 5,500 feet (and training year round up to 14,000), I don’t sleep well above 9,000 feet. For many, ability to sleep at altitude changes as we age.

Climate, altitude, neighbors, convenience, community, quality of local schools/governance… good reasons to rent locally before you buy.

One of the topics from our recent Couples Retreat was vacation property. I needed some time to show-my-work for why I’ve decided to stay variable.

The question, in the context of both buying and not-buying, was…

Will it make a difference?

The question gives me an opening to share some things I’ve learned from 25 years of real estate investing.

1/. I have yet to regret not-buying a vacation property. When vacation markets appreciate, so do investment markets.

2/. The ones-that-got-away have three main attributes: well located, easy to find tenants and decent cash yield. Vacation properties usually only have one attribute… well located.

I’ll share insights about capital allocation:

=> No one in the company is likely to care more about capital allocation than the boss – the CEO sets a cap on how much people will care about capital, and everything else for that matter.

Extend into your marriage, and family….

=> No one will care more about spending and capital allocation than the individual responsible for earning the income/capital in the first place.

Similar to work ethic… the actions of leadership set a ceiling on what to expect. No amount of legal documentation, and pontificating, can overcome this reality.

Don’t waste energy fretting about the way things are.

Be grateful when you’ve been able to create a team that, largely, follows your lead.

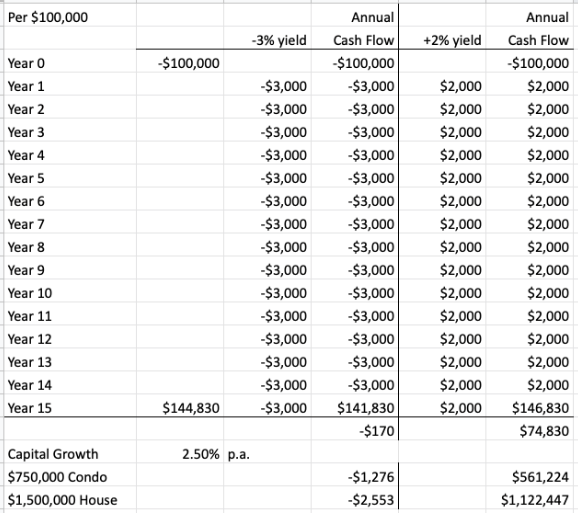

Now the math!

I’ve updated my #s for the two markets I follow most closely.

A vacation market with an effective yield of -3% (cost to own). I avoid fooling myself that I’ll be able to short-term rental myself to breakeven.

An investment market that is generating net cash flow of 2% per annum.

To “get my money back” in the vacation market, the value of the asset needs to grow by 2.5% per annum.

Money back does not mean purchasing power back. The “same” dollars in 15 years time will buy less due to inflation – just look backwards to 2005 in your home real estate market and see what your current place was worth.

We have no idea about what the future holds and 2.5% market growth is probably looking tiny when compared to what you’ve seen over the last year (+30% in my zip code).

You could be right.

I do, however, know markets that are just getting back to their 2008 peaks. In a negative cash flow scenario, that’s a painfully long time to hold.

My goal isn’t to predict an unknowable future. My goal is to answer the question “will it make a difference?”

In the get-your-money-back scenario (2.5% market growth):

Take time to calculate your true cost to hold.

Make sure you’re OK with permanently increasing your burn-rate, especially if there’s debt service.

Know your alternative use of funds => the investment property returns $1.75 for each $1 invested & Vanguard’s VTSAX is currently yielding 1.4%.

The vacation property requires an extra $0.45 for each $1 invested. This is before you decide to renovate and burn $$$s on rugs, curtains and furniture!

For that vacation property, here’s what I do…

Take the purchase cost

Make sure I’m OK with annually spending 5% of purchase cost, forever

Consider if I am OK with writing-off the equivalent of 50% for customization, the cost of ownership and agent’s fees

Then remember:

My personal utilization of past destinations has been 15-45 days per annum.

The future risk to my family is we are priced out of our home market (not that my spouse and kids might have to unpack/pack up from a rental).

I tend to change my mind.

Feelings!

One of the challenges with new deals is my feelings are dominated by the expectation of the asset making things better.

I also enjoy the feelings associated with being able to provide for my spouse and kids.

Making things better & doing right for my family => it’s difficult to feel the benefit of doing nothing.

Once I have a good-enough position, the only person who can screw it up is me.

My favorite real estate can’t be bought – Collegiate Peaks Wilderness Area

Our local property market has popped 30% since the start of the pandemic.

I did not see that coming.

Here’s a key insight => my lack of foresight had no impact on my family => our success does not rely on directional bets.

We establish a good enough portfolio then focus on: (a) keeping our cost of living in line with our cash flow, (b) shared experiences and (c) staying the course.

A recent John Mauldin note reminded me of two components of real estate.

Investment – the potential for reliable cash flow and long term capital gain

To those I would add:

Signaling – an example from my own life. Before my wife was “my wife,” I bought a townhouse in Boulder. It showed her, I was committed to Boulder. It showed her family, I had the funds to take care of their sister/daughter.

Asthetics – worth between “a lot” and “nothing” depending on my stage of life. As I age, increasingly appreciated. I was 50 before I could relate to the concept of a $1,000,000 view.

Community – In my early 30s, I found myself in Christchurch, NZ. The community was an excellent fit for the life I wanted to live (sharing outdoor activities with friends, elite triathlon). The South Island of New Zealand has always felt “right” to me. On the other side of the equator, was Boulder, Colorado. There I found love and decided to establish my family.

I didn’t need to own real estate for love, community or family. some qualities work best when inverted.

Location inverted => The principle here might be don’t invest anywhere your spouse won’t live.

Asthetics inverted => Absent financial duress, locations you can buy cheap tend to stay cheap.

You can extend to secondary markets.

My family loves Vail.

Rather than buying a 40 yo condo for close to a decade’s worth of core living expenses… we allocated 2% of the capital and joined a world-class ski club.

My annual family ski budget, including club and rental housing, is about the same as what the old condo would cost to own. The principle => don’t capitalize luxury expenditure.

I made this decision because I’m not confident about my life 10 years from now – when I’ll be an empty nester.

In making a decision to “not buy” I have maintained: (a) a cheap option to change my mind in the future, (b) I’m still debt free, and (c) my capital is available to be used elsewhere.

About elsewhere… I am very confident that my children are going to be grateful that I kept the family invested in the Boulder real estate market. Hedge the risk your family will be priced out of the place your kids grew up.

Of course, this assumes you are living in a place you don’t want to leave. It’s not just your spouse you should pay attention to…

The above components can work against each other.

For example, signaling vs return on investment. I’ll give an example…

Trophy house was 55 bags of leaves. Current house 5 bags. Little things have a big emotional impact on me. I love low hassle ownership.

After we married, I bought a very large house, not far off the size of a small school. The bills, and constant yard work, took the fun out of ownership. Being a big shot turned out differently than I expected.

This experience nudged me into a principle, apply the minimum capital to achieve the goal and pay attention to the cost of ownership (money, emotion, time).

And that’s really the point I wanted to make.

In a hot market

Consider the need you are seeking to fill

Pay attention to the cost in time, emotion and ownership

Remember that capital is precious and leverage can trap you in situations where a renter can easily exit

If your time horizon is less than a decade then rent

All of this is easier to see when you’ve been through a few recessions. At the start of 2009, I promised myself to never opt-in to avoidable financial stress.

The tough part is building the capital and credit capacity to be able to buy.

Whatever you were seeking to achieve, you achieved it BEFORE you purchased.

The easiest time to build capital is in your 20s. You can live very cheaply because you’re either at work, or carousing. Your health insurance is peanuts and you don’t need to take on any dependents (free birth control saves lives).

Age is not a barrier. Use the recipe below and you can be living free by 2030.

Big Cities remain the best places to build experience, knowledge, contacts and skills.

When I made partner, a wise man took me out to breakfast and reminded me…

Get what you want, then get out

He didn’t tell me why I needed to get out. I learned that for myself…

You’ll be jammed into a little place and/or you’ll have your financial life tied up in a single asset – you won’t care about this after graduation, you will care about this when you have preschoolers!

It requires extreme luck to get yourself on the housing ladder before you’re 40 => get your timing wrong and you’ll feel trapped

You will be surrounded by social pressure to spend, spend, spend!

Megacities are filled with opportunity and excellent people to whom you sell your skills.

Megacities are a great place to start.

Just remember to leave.

Target Location

Having played this game three times, I think a small city is your best bet.

~250,000 (pop.) in a county with ~500,000 (pop.)

Natural Beauty – clean water, clean air, the ability to exercise safely without driving

Climate – I gamed this by having a rental in the Northern Hemisphere and a low-cost Home Base in the Southern Hemisphere. Later in life, I moved to a place I didn’t need to leave (Colorado, Front Range)

Airport Proximity – needing to take a flight-to-your-flight will get old

Before my first kid was born, I worked in: Canada, England, Hong Kong, New Zealand, Bermuda and Scotland.

The skills to be happy somewhere are the same as the skills to be happy anywhere.

Target Property

My worst deals (financially) have been the most impressive (visually).

Buy space and let the next owner spend a fortune in renovations. The money I’ve spent beyond paint, carpets and replacing worn out appliances/HVAC has been largely wasted.

You’ve probably spent the last decade renting – your younger self is your target market. Choose a location that will be easy to rent (if you leave, if you need income).

Lock off basements, detached units, split floors… earn rental income, maintain personal privacy.

Margin of Safety – your land premium is “total price” less “value of the buildings” – the closer you get the land premium to zero, the safer your deal.

Coming out of the Great Recession of 2008, land premium was briefly negative – this was due to banks foreclosing and forcing the market down. Five bedroom houses, 15 minutes from Boulder, were selling at $75 per sq foot. Condos, apartments and houses in Arizona got even cheaper, under $50 per sq. foot.

Cheap will happen again.

Connection

It can be tempting to go remote. I feel ya.

Escapism is a recurring dream of mine, especially in times of stress. However, you need to be practical – friends, sexual partners, basic services, transport… the practicalities of life.

The purpose of setting up your low-cost base is to provide security within a life with meaning. Go to where there are people with whom you’d want to spend the rest of your life.

Shared values, within an active lifestyle.

Wait For The Fat Pitch

To get this done you’re going to need a trigger that makes the local property market seem cheap to YOU. It won’t seem cheap to the locals, who will be expecting further declines.

Recession combined with High Interest Rates (UK 1990)

Asian Crisis (1997)

Currency Crisis (NZD in 2000)

Global Financial Meltdown (2008)

I witnessed all of the above. There is ALWAYS a “next crisis”.

2020 was a boom year in real estate. When you’re living through a boom, your FOMO will be pushing you to take action.

One of the best things your first good deal brings you is a reduction in the pressure to do a deal.

To do great deals, you need to be comfortable doing no deals.

I’m going to chat you through the financials of a rental property I used to own in Tucson.

This will help you understand the situation facing airbnb hosts and other owners of assets with high holding costs.

Picture a condo, bought and furnished for $75,000.

The condo has a current value of $100,000.

The condo doesn’t have a loan against it but costs $8,500 per annum to hold (8.5% of value). The high cost to hold is due it being a fully furnished rental => things like taxes, HOA, cable, insurance, utilities…

The furnished rental does great and yields net cash flow of $4,500 per annum after all expenses, taxes and commissions => 6% of cost.

This was a good investment but I sold out, and switched into Boulder real estate, with a mortgage. Here’s what I switched into:

Cost to hold the house (mortgage, taxes, insurance and maintenance) => 3% per annum vs 8.5% for the condo. Without the mortgage, the cost to hold the house drops to 1.25%.

Worth emphasizing the debt-free annual cost to hold comparison => condo 8.5% vs house 1.25%

House has rights to land, condo doesn’t include any land rights.

House has alternative uses… can live in it for the cost to hold, or rent and receive a net yield of 1.5% (2.75% excluding the mortgage).

Both locations worked out.

I checked on the condos yesterday and they were selling at ~$150,000 pre-virus, up significantly from 2008-2010 crisis values. Boulder housing has seen similar appreciation.

What concerned me in 2012, when I sold, was the high cost of ownership, which can bite in a downturn.

Picture the condo debt financed => this is the issue facing aggressive airbnb hosts

A $75,000 purchase, with a mortgage of $65,000 against the property

To buy the place, you needed $10,000 of equity, which appreciates to $35,000 as the capital value rises (on paper) to $100,000.

The paper profit is 3.5x your money (yay) => you get this from 33% market appreciation, similar to what has been seen in many markets over the last 3-5 years.

But… the Virus pops up and the property is going to cost you $7,500 of new cash to hold for the 1st year of the crisis => 7,500 / 35,000 is a negative 21% return on equity.

All of a sudden, the warm feeling of paper profits is replaced by the reality of writing checks, monthly, for a vacant rental.

Depending on your tax bracket, one year cost to hold might be the equivalent of the last three years profits.

+++

The high cost to hold can bite in different situations.

Club Memberships => $50,000 to $250,000 membership initiation fees with annual dues of $5,000 to $25,000.

You can find yourself in a contractual relationship where you are required to pay 5-20% of membership value in a downturn.

Now picture a club with 10-20% of the membership unemployed, or ill with COVID.

+++

In a world with: (a) very low discount rates; and (b) professional compensation under pressure, the “penalty” for paying through a downturn/crisis is accentuated.

Many asset owners are likely telling themselves they are simply facing “one bad season” and things will get back to normal soon.

You must be logged in to post a comment.