Back in Feb, I laid out ideas for Multigenerational Capital, it included my strategy of Sell, Buy & Hold.

Last week, I completed the Sell Goal for 2022. There are two numbers I’d like to revisit:

- Gross Yield of 43 years, 2.3%

- Net Yield of 64 Years, 1.6%

I gave up ~2% yield on capital to add to my Strategic Reserve.

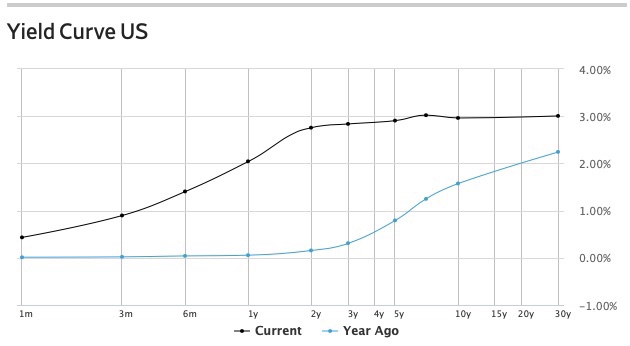

Snapshot from last week:

- 2Y to 30Y yield ~3%

- 30-year mortgage 5.25%

- VTSAX Dividend Yield ~1.5%

By the end of 2022, short-term margin debt is expected to cost more than index equity yields. Medium-term debt is already more expensive.

These changes mark an end to the free-money policies of the last few years. This is a big change – it is unknowable if the change will prove sticky.

So… wait and see. I did a minor rebalance this week.

The rebalance was a repeat of the “buy less” strategy I shared in Feb.

In March 2020 I increased equity allocations to 72% of my Vanguard portfolio.

Allocating additional capital in 2022, I made a reserve for “an investment that benefits the present”…

…then rebalanced to 60% equity allocation.

This reduced the size of the new investment and got me past decision paralysis, driven by a fear of near-term loss.

The reserve now sits at ~15 years Core Cost of Living.

We’ve been looking around for a place in the mountains.

Coming off a year of AirBnB skiing, I know our cost to rent implies a gross yield of 0.75 – 1.75%.

Alternatives to buying:

- Stick the Strategic Reserve into VTSAX, rent through AirBnB and let dividend growth hedge rental inflation

- Stick the Strategic Reserve into a medium term bond product (VBTLX @ 3%) and earn a margin over my cost to rent

- Pursue either of the above, double my discretionary spending and run the capital down between now and my wife’s 85th birthday

For now, I’m taking Door #4

- Rebalance after large (down) moves

- Watch the Federal Reserve increase rates

- See what happens

A 35% market decline implies a dividend yield over 2.25%, which would let me lock in the equivalent of three-months cost of living (after tax, forever).

I tossed my idea of buying a Sprinter Van for camping. The shift towards “assets for fun” doesn’t come naturally.

You must be logged in to post a comment.