I had a friend ask me if I thought “cash is king” in the current environment. My answer is more than can fit in a tweet so here you go.

Key Point: when we read reports of monetary policy tightening, I think we are being misled. On a historical basis, policy remains accommodating.

The collective is lousy at remembering history.

The value of everything, in the world, has been inflated by the actions of Central Bankers. I think everyone accepts that point. Thing is, it is impossible to measure the scale of the inflation.

In recent memory, the best example will be to cast your mind back to when crypto was a one-way bet.

Asset inflation feeds upon itself, until it doesn’t.

The increase in the size of the Fed’s balance sheet has been a strong tailwind and dominates our collective memory.

If you’re 35 and under, then unprecedented monetary inflation is the only environment you’ve ever known.

Time for another chart.

Here’s a chart of our current reality (black line).

We’ve lived the rate increase, but assets prices have not adjusted to the new reality.

Why?

- The economy is rolling along – the tailwind was powerful, and strong

- It is unclear where the Fed’s massive balance sheet is going – there has been 13 years of QE – who wants to bet against another round, I don’t

- There remains plenty of OPM (other people’s money) and leverage

VTSAX Yield (1.5%), VBTLX Yield (3.4%), VMFXX Yield (2.1%)

Those are equity, bond and money market funds I track, as at last Monday.

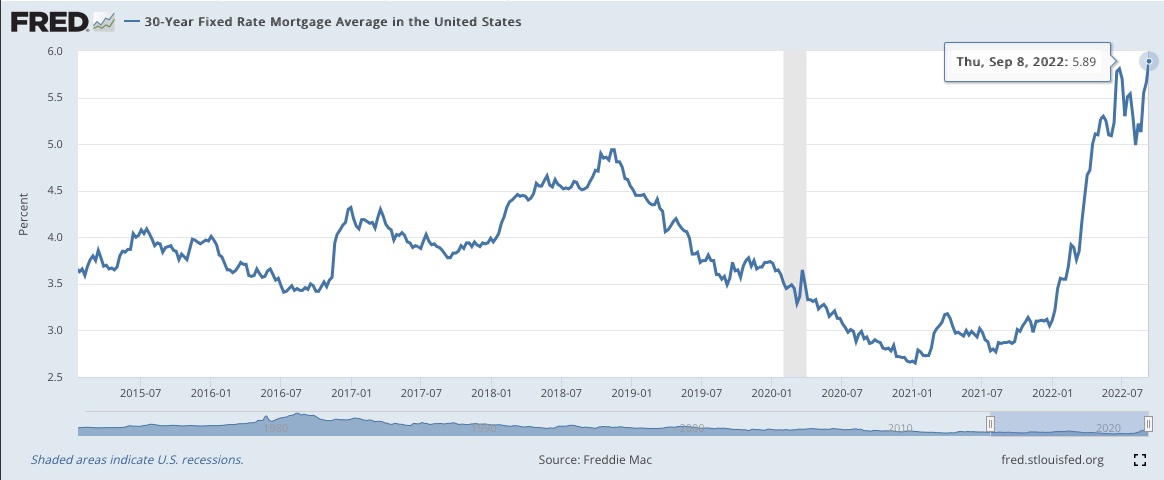

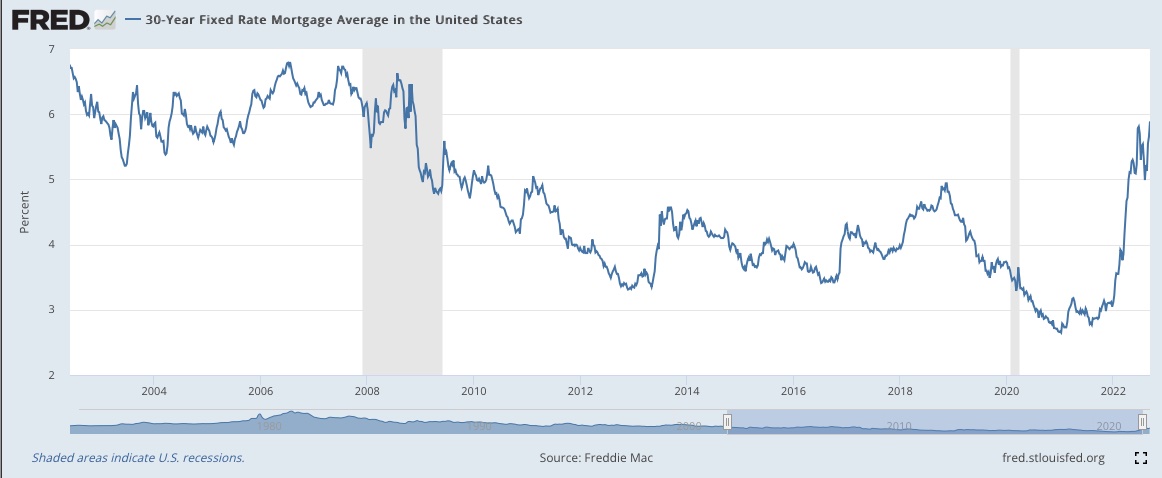

Mortgage rates appear to have jumped.

However, let’s have a look at the next chart.

Rates are only just getting back to their 2003-2008 level, a time when people were hardly holding back on real estate.

So what do I think:

1// Assets could get cheaper – I don’t see any case for a melt up.

2// If the Fed materially shrinks their balance sheet then assets will get a lot cheaper. Cutting their balance sheet in half takes us back to 2015.

3// Sit down and ask yourself “what if” asset prices drop to 2015 levels, a 50% reduction. Odds are, you have your interest rates locked in. So the main risk will be short term cash flow due to unemployment. How might you protect yourself?

4// Having a year’s core cost of living in an “emergency” fund makes sense. Personally, I didn’t reinvest the proceeds from a Q2 asset sale. My reserve is enough to navigate a nasty recession without selling anything further.

So a “prudent cash reserve” is King.

I don’t think it makes sense to liquidate positions, and pay extra taxes, because risk assets might fall in value.

I do think it makes sense to look at family spending and see the allocation between: essential, discretionary and luxury. The ability to adjust spending downwards is a useful hedge in an unpredictable world.

Keep living and sharing experiences with those you love.

Time and shared experiences are true wealth.

You must be logged in to post a comment.