I started thinking about this with negative-yielding sovereign bonds. When something makes no sense to me, I pause and reconsider my assumptions.

The phenomenon, of not being able to understand buyers, has now spread across markets and asset classes. In markets I know well, I’m being out-bid by 20-25%. Missing by a lot, makes it easier to sit out.

The goals and incentives have shifted, and it’s taken me a long time to notice.

A big chunk of global capital sits as a hedge against the value of money declining. A decline in the value of money:

- is not a risk for anyone rich in youth and skills

- is seen as a risk for the financially wealthy – a very human trait of worrying about wealth that’s far above one’s requirements for a meaningful life

Over my lifetime, we’ve shifted to a society where wealth is controlled by:

- People managing Other People’s Money, with access to debt and options on gains

- Fewer and fewer people, managing more and more money

Toss in near-zero rates and we’ve reduced the incentive for investment discipline.

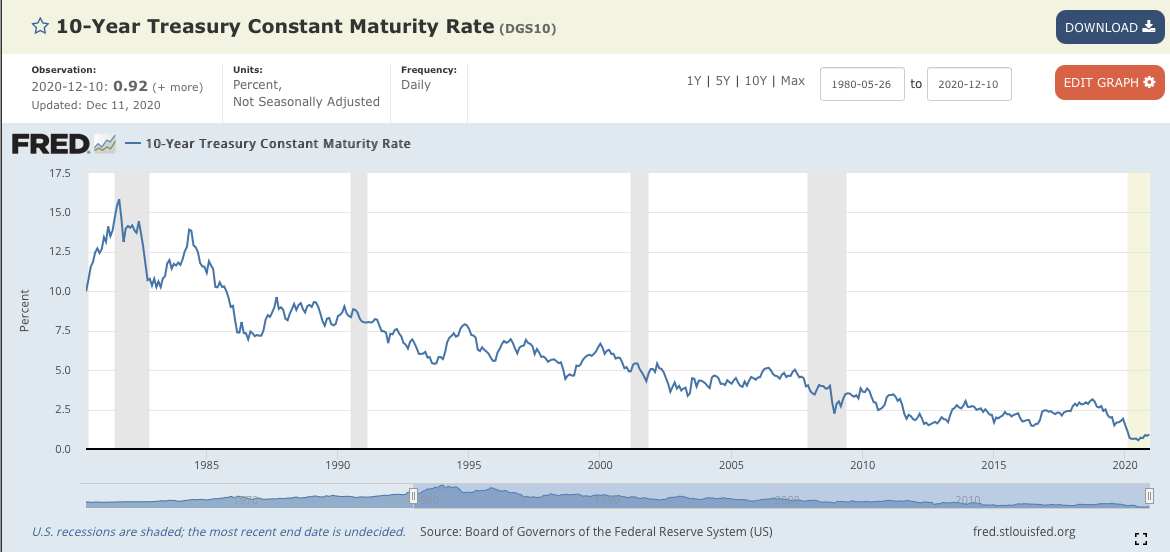

A shift away from treasuries is painful when they are yielding over 5%. Less so, today. The shift in attitude has happened very slowly – it took more than a decade.

For a species that worries about $4.99 shipping charges (when they save TIME from leaving the house)… Cash Returns Matter – the absence of cash returns gives an incentive to devalue safety.

With negative 10-year (!) rates, the European incentive (to flee safety) must be extreme.

It’s emotionally easier to own marginal assets when cash yields nothing (and you are seeing paper gains across most asset classes).

Risk has been rewarded and reinforced across a generation, maybe two generations.

While it started with good intentions, recent monetary policy has had the unintended consequence of rapidly inflating the assets of the already (super)wealthy. When I think about the resulting incentives for risk tolerance, government spending and borrowing, that strikes me as bad policy.

I’ve no idea how, or when, this play out. Fortunately, I’ve set my life up so I don’t need to be correct with uni-directional bets.

Careful with margin-debt and recourse leverage, it’s been one heck of a run.

With yields this low, there is tremendous leverage built into the system.

I’ll be back posting in 2021 – it’s been a solid year of writing.

Thanks for reading.

You must be logged in to post a comment.