I graduated from university in the summer of 1990. I didn’t know it at the time but it was an excellent time to start a career in finance.

The price of money has been falling ever since I graduated (1st Class Honors, Econ/Finance, McGill). My first real finance job was the most junior member of a very successful private equity team in London.

It doesn’t enter into popular consciousness but many of us have had the benefit of a 30-year tailwind. This tailwind impacts every aspect of our lives and, like oxygen, we’re largely unaware of it (while it continues).

For the first half of my finance career, a modest interest rate cut was sufficient to get everyone excited.

At this stage of the cycle, it takes a healthy dose of shock & awe to move, or steady, the markets.

It’s important to remember:

- It is impossible to know the future in real time. If you find yourself saying the Fed is making, or not making, a mistake then you’re fooling yourself.

- It is possible to assess the risk in the system => leverage, debt service, off-balance sheet liabilities, derivatives obligations, debt:equity ratios, months of cash on hand vs monthly cash burn rate… there are a lot of useful measures. You should know these measures for your country, state, county, firm, family and self.

I don’t want to comment on right or wrong. I simply want to share observations that, hopefully, will help you think better about money.

In my line of work, I hear a lot of themes.

I’ll share a couple themes and my counter-dialogue.

The market is so high, I need to sell or I will lose money.

- Volatility isn’t loss – come back to this one in the next down cycle.

- Constantly tracking the price of anything will cost you time, lower your return and lead to misery. See Fooled By Randomness, by Taleb, for the best explanation of why you should ignore the volatility of a good-enough portfolio (or life for that matter!).

- My entry prices are 30-60% below current market. Instead of focusing on a fear of loss, I focus on the cash flow being generated from wise past decisions.

- If you exit then you need to put the money somewhere. The benefit of a good position is you don’t need to figure this question out. The less I need to think, choose and act… the better.

- Every positive action costs expenses, taxes and introduces the possibility for error.

- Most the people who worry about money, don’t need to worry about money. Beware of using financial news as a distraction from what you really should be doing with your life.

Price vs Happiness vs Wealth

- Price is an illusion – all assets move in cycles.

- Price changes are not wealth changes.

- If you build a habit of happiness with price increases then you will experience a multiple of pain with the inevitable declines.

- Equanimity must be trained, and re-trained.

- Financial wealth comes from productive capacity, which is the ability to give the world what it wants.

- What does the world want? My world wants…

- Cash flow generation

- Saving time

- Reducing hassle

- To survive

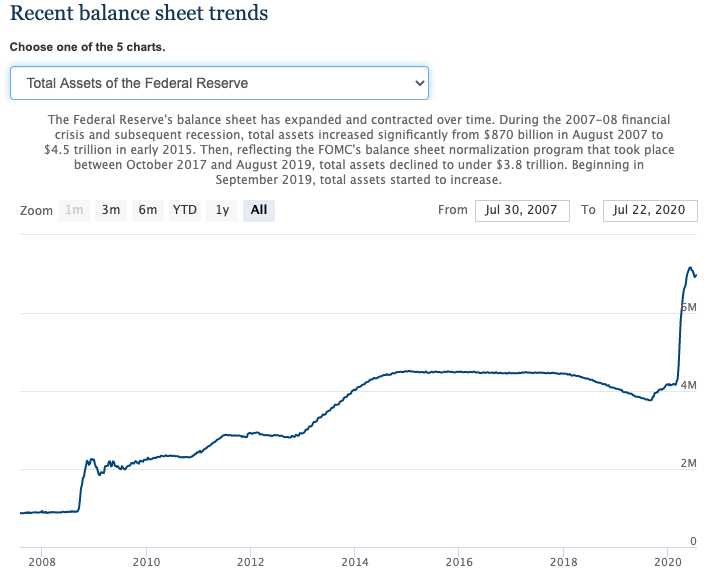

When you create a lot of money (see chart above and, note our constant, longterm Federal stimulus), the money needs to go somewhere. When money “goes somewhere”, especially when debt is available on top, prices go up.

The effect is not wealth creation, the effect is asset price appreciation.

The first principle is that you must not fool yourself – and you are the easiest person to fool

Feynman’s rule on foolishness

In 2020, all this money creation might be saving us from disaster. At best, we’ll get a chance to argue in hindsight.

Don’t fool yourself by acting as if your wealth has been increased.

The risk in the system has been increased.

You must be logged in to post a comment.