A friend asked how to gain equity exposure via the stock market.

I recommended John Bogle’s Book and shared what I do for my own family.

Decide what pot of money to invest – in order of priority

- Tax deferred retirement accounts for me and my wife

- Tax deferred 529 accounts for my kids’ education

- Taxable investment accounts for my family

In Colorado certain 529 accounts also have the benefit of a 1-for-1 deduction from state taxable income in the year of investment. However, the 529 accounts have a higher expense ratio than the funds I access for our retirement accounts (0.45% vs 0.05%). The Colorado state income tax rate is 4.63% so the tax savings helps me justify a higher cost.

For #1 and #3 I prefer to use Vanguard’s Admiral Shares for their Total Stock Market Return Fund (VTSAX) – it has an expense ratio of 0.05%.

I always compare expense ratios for products. For active managers, and fund-of-funds, make sure you get the total expense ratio that looks all the way through the final investment products. Many advisers have a financial incentive to layer fee-generating products and you may have additional taxes due if your portfolio has a lot of (largely unnecessary) churn.

It is important to remember that most people lose the majority of their return via investment churn, taxes and expenses.

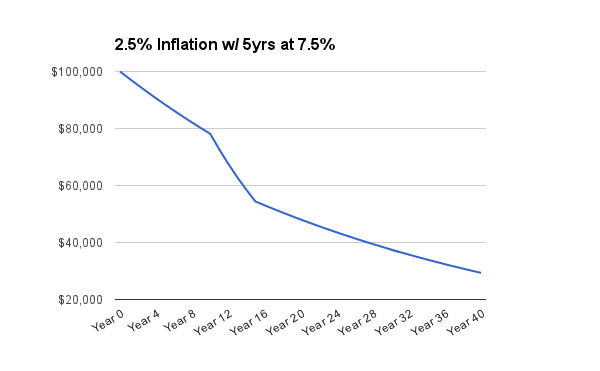

Let’s use an actual case study with numbers…

If I wanted to invest $100,000 then I’d move into the position gradually with a fixed dollar amount of VTSAX purchased each week. An example would be $10,000 initial investment (to qualify for the Admiral Shares) then $360 automatically purchased every Wednesday for the next 250 weeks. Five years later, you have your position.

The toughest part about the above strategy is leaving it alone. There will be times when you want to invest more, or less, depending on the emotions involved with following the market. Research shows that our emotions are lousy investment guides. So…

My recommendation is to set the automatic investment at a level that you can sustain FOREVER and leave it alone. Let surplus cash build up in another account and use that for opportunistic investing.

Don’t believe the fallacy that you need a portion of your portfolio “for fun.” The purpose of investing is to earn a return on investment, period. When I want to have fun I go for a bike ride with my pals, I don’t speculate with my family’s capital.

When I do a portfolio review, I look at my total exposure by $ amount and asset class. I review the position “right now” as well as how the position is likely to change, based on future investments, earnings and expenses.

If I’ve lost you at this point then you’re not alone. Sitting down with a financial planner can be extremely valuable. Make sure your adviser makes money by advising you, not selling you products. Firms, like Vanguard, offer financial planning services for a very reasonable fee.

Last week, I shared that I felt over-invested in Real Estate so I’ve made a decision to reduce my holdings. Once I’ve reduced my exposure to real estate, I need to figure out what to do with the cash. Today’s blog post is one option (buy equities over five years). Another option is do “do nothing” and wait for the next crisis. It’s really hard to “do nothing” so, perhaps, I’ll do something really slowly and buy equities over 10+ years.

A long range projection of your family finances (5-10 years) is useful to figure out what dollar amount it makes sense to invest. Consider if you want to retain cash for opportunistic investments: examples might be starting a company; buying investments in a crash; or buying real estate in a recession. In my own life, a handful of opportunistic deals have been what made a difference to my portfolio. These deals were made possible by the ability to deploy cash quickly.

Consider a cash reserve to cover unexpected illness or unemployment. Here’s my post on Lifestyle Insurance. Over and above insurance products, I feel better when I have at least one year’s gross expenses held as a cash reserve. In terms of life changing financial security, here’s my post on Taking Money Off The Table.

I’ve yet to regret selling early – I’m easily frightened by bull markets. A recent trip to the Bay Area set off all kinds of warning bells!

What I’ve described is more generally known as “dollar cost averaging.” John Bogle’s book explains how to use this strategy to give yourself financial security. Highly paid professionals (dentists, doctors and lawyers, particularly) are prone to exploitation by my peers in the financial services industry. Read the book.

A bull market is an ideal time to pause, take stock and ponder long term positions. Right now is when it’s most easy to adjust portfolio strategy.

You must be logged in to post a comment.