One of the topics from our recent Couples Retreat was vacation property. I needed some time to show-my-work for why I’ve decided to stay variable.

The question, in the context of both buying and not-buying, was…

Will it make a difference?

The question gives me an opening to share some things I’ve learned from 25 years of real estate investing.

1/. I have yet to regret not-buying a vacation property. When vacation markets appreciate, so do investment markets.

2/. The ones-that-got-away have three main attributes: well located, easy to find tenants and decent cash yield. Vacation properties usually only have one attribute… well located.

I’ll share insights about capital allocation:

=> No one in the company is likely to care more about capital allocation than the boss – the CEO sets a cap on how much people will care about capital, and everything else for that matter.

Extend into your marriage, and family….

=> No one will care more about spending and capital allocation than the individual responsible for earning the income/capital in the first place.

Similar to work ethic… the actions of leadership set a ceiling on what to expect. No amount of legal documentation, and pontificating, can overcome this reality.

Don’t waste energy fretting about the way things are.

Be grateful when you’ve been able to create a team that, largely, follows your lead.

Now the math!

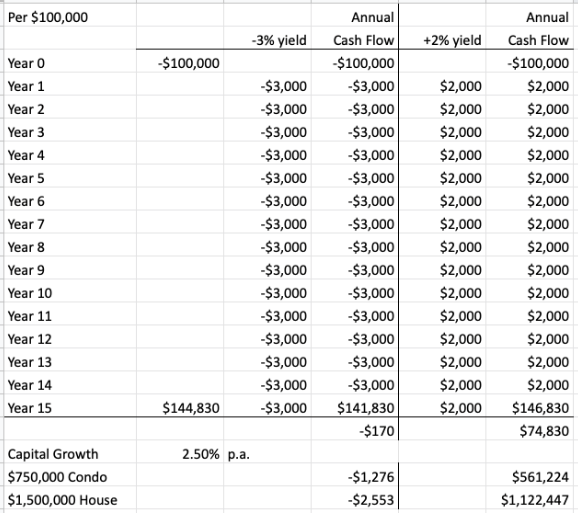

I’ve updated my #s for the two markets I follow most closely.

- A vacation market with an effective yield of -3% (cost to own). I avoid fooling myself that I’ll be able to short-term rental myself to breakeven.

- An investment market that is generating net cash flow of 2% per annum.

To “get my money back” in the vacation market, the value of the asset needs to grow by 2.5% per annum.

Money back does not mean purchasing power back. The “same” dollars in 15 years time will buy less due to inflation – just look backwards to 2005 in your home real estate market and see what your current place was worth.

We have no idea about what the future holds and 2.5% market growth is probably looking tiny when compared to what you’ve seen over the last year (+30% in my zip code).

You could be right.

I do, however, know markets that are just getting back to their 2008 peaks. In a negative cash flow scenario, that’s a painfully long time to hold.

My goal isn’t to predict an unknowable future. My goal is to answer the question “will it make a difference?”

In the get-your-money-back scenario (2.5% market growth):

- Take time to calculate your true cost to hold.

- Make sure you’re OK with permanently increasing your burn-rate, especially if there’s debt service.

- Know your alternative use of funds => the investment property returns $1.75 for each $1 invested & Vanguard’s VTSAX is currently yielding 1.4%.

- The vacation property requires an extra $0.45 for each $1 invested. This is before you decide to renovate and burn $$$s on rugs, curtains and furniture!

For that vacation property, here’s what I do…

- Take the purchase cost

- Make sure I’m OK with annually spending 5% of purchase cost, forever

- Consider if I am OK with writing-off the equivalent of 50% for customization, the cost of ownership and agent’s fees

Then remember:

- My personal utilization of past destinations has been 15-45 days per annum.

- The future risk to my family is we are priced out of our home market (not that my spouse and kids might have to unpack/pack up from a rental).

- I tend to change my mind.

Feelings!

One of the challenges with new deals is my feelings are dominated by the expectation of the asset making things better.

I also enjoy the feelings associated with being able to provide for my spouse and kids.

Making things better & doing right for my family => it’s difficult to feel the benefit of doing nothing.

Once I have a good-enough position, the only person who can screw it up is me.

You must be logged in to post a comment.