I was going to take a break from posting but this topic gives me an opening to share something useful with you.

So here goes.

First, I know next to nothing about crypto.

Fortunately, my life has been set up to take into account that I am clueless about many things!

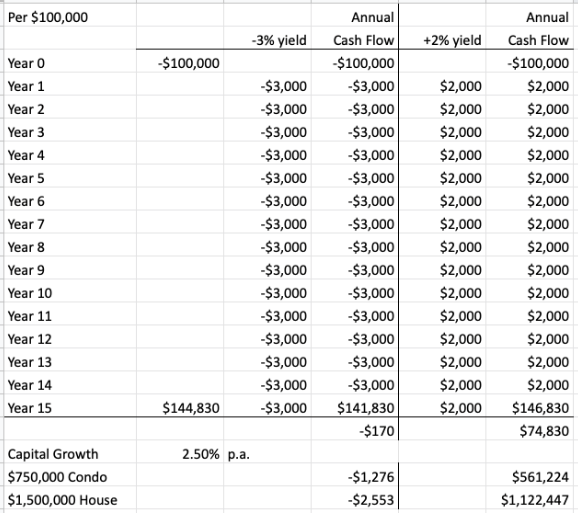

I think we can start by agreeing that crypto is volatile.

So I’d suggest you start by thinking deeply about how you, your significant other, your family and your coworkers tolerate volatility.

I don’t need to think deeply. My family abhors volatility. They get nervous about stuff we don’t own.

Personally, I tolerate volatility but tend to sell early. By way of example, I am absolutely certain that I would have sold Amazon 20+ years ago. Grateful I didn’t short it.

So, regardless of the fundamentals, I’m not a good fit for the asset.

About those fundamentals, I can’t see them.

I could learn about crypto but, while learning about an asset class that isn’t a good fit, I am not working on something else.

Let’s repeat that… while thinking about one thing, I am not thinking about another thing.

The opportunity cost of mis-directed thought.

Say I get there – I’m comfortable with the asset class, and I’ve gotten myself and my investment committee past the volatility issue.

Will it make a difference?

Buying, not buying, selling, not selling. Being right will not make a difference in my life.

The opportunity cost of incorrect focus. Big one.

If asset classes don’t make a difference then what does?

I was thinking about this on my run this morning. So let’s start with that… dropping fat, maintaining a stable weight, daily movement in nature, improved strength… big difference!

Since shifting my primary focus away from money, my body has had the opportunity to do a lot of cool stuff.

Trying to get more, of what I don’t need, can prevent me from getting something useful.

Leaving => I wrote about considering if an asset is a good fit for an owner. What about life?

Leaving makes a difference.. every single time I realize I have different values than my peers, I exit => patiently, quietly, doing a good job on the way out.

I need to watch this tendency. Making a habit of leaving is not going to take me where I’d like to go. Stay where I belong.

Building => Don’t look for easy money, build something.

I helped a friend build a business. Unfortunately, he lied to me and stole money from the investors. Interestingly, when the dust settled, that didn’t make a huge difference. If someone isn’t trustworthy then it’s better to know, as soon as possible. In the end, I learned a lot and walked away with 25-years living expenses.

Learning, while building capital => made a difference, up to a point of rapidly diminishing returns.

As you age, I recommend you transition your focus from money to relationships. Because…

Family => marrying well, raising my children to be exceptionally kind and athletic… makes a huge difference, much more than spending the last ten years building wealth would have done.

Having the courage to change, so my kids’ values are a better fit with my own.

We tend to over-value what we see.

We see crypto rocketing and we think it must be a good idea. It might be. Like I said, I know nothing about it.

But what we don’t see is often more important.

Thinking about that on my run… the decision “to not” has helped in ways I will never see.

Errors not made.

Not smoking, not using scheduled drugs, not taking sleeping pills, not giving into anger, not quitting…

1/. Will this make a difference?

2/. Will “not this” make a difference?

A useful filter on where to focus, and what to avoid.

You must be logged in to post a comment.