My kids won’t fully appreciate my choices until after I’m gone.

My #1 financial goal for my kids is debt-free education in a field that enables them to get paid.

With the very best of intentions, the US Government has completely screwed up both (a) the cost of college education and (b) the financial lives of the students they were seeking to help.

Debt isn’t free.

Every market juiced with easy money gets screwed up.

Explanation below – my life mirrors the blue line – graduate early, debt free, start saving

I googled up average debt at graduation and average graduation age.

$40,000 and 23 yo.

So let’s make three simple scenarios:

Debt free early graduation (21 yo) => McGill 1990 finance grad

Debt free at 25 yo

Debt free at 30 yo

Let’s run it forward assuming:

Investment return of 5%, prior year close

$20,000 per annum savings

The late-start saver

who saves at the same annual rate

who earns the same return

ends up ~$1 million behind at 60 yo.

This is not the whole story, not even close!

In my demographic, families can burn ~$250,000 of capital to help a kid “get started” => 529 accounts and parental support. Even more if you roll private from Kindergarten.

What’s the 30-year cost of this choice?

$250,000 * (1.05)^30 = $1,080,000

Million bucks gone, you never see it.

You burned the capital

The kid figures life out by 30, and spends most of their 20s pissed at you (for tapering their support) 😉

$2 million opportunity cost, spread between two generations.

You assume it was what you were supposed to do and are grateful you finally got them off the payroll.

A possible alternative…

Our default position is in-state education and I’ll buy whatever’s left of your 529, at $2 on the dollar, once you save $100,000 of your own money.

That article introduced the concept of Lifestyle Sustainable => a low-cost base of operations where, ideally, you can live for free. The idea is to remove cost-of-housing from your financial concerns.

That’s the core financial asset for your portfolio. It cost me US$110,000 in 2000.

This is a great place to park your Core Capital.

Removing housing from your list of concerns gives you more than a financial return.

Alongside your key financial asset, I hope you have a loving, lifelong partner. This person is the most important decision, financial or otherwise, you’ll be making.

The highest return investments I made in my 30s & 40s, were not financial in nature. With a low-cost base of operations, & marketable skills, I was in a good place.

Many high-earners fail to see the value of what I just pointed out.

Low-cost base of operations

Marketable skills

Beyond that, most everything is lifestyle enhancement and ego.

Thankfully, I had a major setback in my early-30s (divorce) which gave me pause.

In 2000, I saw my future in front of me… lifestyle enhancement and ego… and I made a change.

A big one.

I became a world-class athlete. With (athletic) success came the realization that something was lacking.

So much success, still lacking!

If you’re good at making money…

If you’re good at playing the game of “career”…

If you are nearing the top of your field…

…then you’ll be tempted to keep doing what you are good at.

I’d encourage you to establish that low-cost base of operations, then try something really challenging…

The highest return investments I made were improving my suitability for marriage and learning how to parent. Most of my learning happened after I was married and my kids were born.

It is never too late to invest in the human capital of your family.

If you get these investments right then you might not notice the benefits. Honestly, a big driver in my life has been a fear of getting divorced again (not-divorced, winning)

Fear that drives positive action is useful.

I’ve been paid by less drama, and less problems (we don’t see all our wins).

I’ve also de-risked some of the challenges my future self will face (companionship, engagement, dementia). Study (the problems of) who you are likely to become.

You’ll notice my portfolio advice (still) doesn’t talk about asset allocation.

This is deliberate!

Asset selection is not the differentiating factor for a life well lived.

Marketable skills

Low-cost base of operations

Fixed-rate mortgage, if you like

Target date fund for your future self

Then focus on living your life and creating the friends/family with whom you’d like to share it.

I was taught that all my (financial) problems would be solved if I made enough money.

Money, absent saving, doesn’t work.

Spending, absent reflection, creates golden handcuffs.

Living a big-city lifestyle had my younger self trapped. His large spending created a hurdle that would have taken him years to overcome.

Valuable years!

Put another way, the weight of my spending was preventing me from launching towards my true self => meeting a wonderful wife and creating my current life in Colorado.

My solution was simple

Save half my take home pay

Get myself to a low-cost environment

Create independent income streams to cover my cost of living

Surround myself with people who lived my values

All well and good, and my 30-something self got some things right.

What he wasn’t able to see was the Window of Time. It didn’t matter to him because he was rich in time, and knew it. Having his basics covered, he risked time on changing direction.

For the prudent, the march of time will eventually require a change in approach.

Each of us is free to change our approach at any time.

At some point, all of us are going to realize that our wealth in time is approaching the point where we have more wealth than time.

This is most likely to occur in what we call the “peak earning years.”

It’s really hard to change direction when you’re coining it.

I know, I did.

Cutting spending, leaning into saving, buying an extra couple years before I’m old…

…all trades you should consider.

Even if you don’t change your path, knowing that you could will strengthen your ability to act with integrity.

So the two landmines I hope you avoid are:

Peer-driven spending that leads you away from what fills your heart

Creating capital for future family members, when they’d rather spend time with you now

I am going to show you how to connect spending, time and wealth.

Let’s bring back my 20-something self. He was living in London, working in finance and renting a room to keep his overheads down.

Coming out of college, having more cash flow than he needed, he felt rich.

But was he?

He earned $75,000 and was spending $32,000. How wealthy was he?

Remember from last week, his net worth was $20,000.

Net Worth “divided by” Spending = WEALTH IN TIME

His WIT was 7 ½ months.

Roll forward to my early 30s. I’m a young Private Equity partner and hit $1 million net worth.

I was spending $250k a year, felt flush, but was I wealthy? Let’s find out.

$1,000,000 / $250,000 = 4 Years

Not wealthy, especially when you consider my life expectancy (>50 years).

++

At 31, I realized my spending was buying me NOTHING. What I liked to do was swim, bike and run. I had fantasies of leaving the corporate world. I took action.

I applied to emigrate to New Zealand. Arriving in Christchurch, I was able to buy a five-bedroom house for US$110,000. My cost of living plunged to $25,000 (NZ$60,000).

My WIT jumped to 40 years.

I didn’t return from my leave of absence. Most of my family thought I was nuts.

When I moved to the US, I went from a 5 to 30% tax rate.

Why move?

Because it saved me money.

Taxes are one slice of your family budget

I used to live in Hong Kong, a low-tax part of the world. Thing is, it’s a high cost location – especially for school fees and residential housing.

Landing in in the US, I chose a part of the country with an excellent public school system. With three kids, that choice saved me a lot of money.

But there are trade-offs.

I grew up in Canada and my family’s basic healthcare needs were covered by the provincial government.

Not so in the USA.

My insurance, HSA contribution and dental cleanings mean I pay $25,000 before anyone’s gotten sick.

I run the $7,000 HSA contribution down against my family’s $14,000 deductible.

Anybody breaks a leg, I’m quickly over $30,000 for the year.

Still cheaper!

In my last year in Hong Kong (2000) I was living in a place that cost $100,000 per annum to rent. The senior partners paid 3-5x that amount.

School fees: friends pay up to $50,000 per kid, per annum. Mine go to public school, a $75,000 saving.

Taxes are the price we pay for living a wonderful life.

Clean air, pleasant climate, easy access to nature, an ability to avoid traffic.

As a friend pointed out, all those Californians moving to Austin are going to find out something… they’re still complaining about taxes, it’s hot as stink, they’re sitting in a traffic jam AND they lost the benefits of living in Cali.

The ability to escape tax policy is 100% in our hands.

Here’s the game.

Take your tax bill and divide it by your net worth.

In my mid-20s, I worked in London. I earned $75,000 and paid $18,000 in taxes. My net worth was $20,000. My tax bill represented 90% of my net worth.

A change in tax policy, or a move to Hong Kong, would have a material effect on my family finances.

Most of us, can’t change hemisphere’s for work.

Many of us, can work remotely from a lower cost location.

Go deeper.

Consider time.

My former self, he saved 50% of his take-home pay from 1990-2008.

We are going to play a ten-year game, the purpose is to build an EMOTIONAL attachment to the power of compounding.

You’re going to need the emotional attachment to counter the impulse to spend what you have.

++

The best way to play is to check your portfolio no more than once a quarter. My kids have gone close to a year without asking me to update.

Give the game YEARS to play out, eventually your students will be amazed.

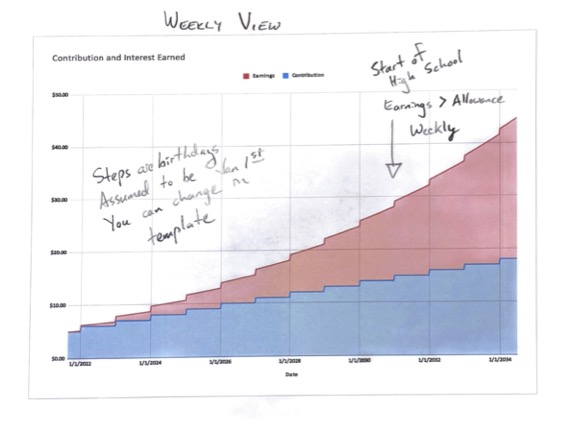

Like a retirement account, not much happens at first. By Middle School the weekly split is $13/$8 between Allowance/Earnings. By HS Graduation the split is $18/27. Game costs you $14K to fund over 13 years.

Investment: each Monday, each player gets $1 for each year they have been alive. I started my kids in Kindergarten so we kicked off with $5 or $6 per week.

Return on Investment: the “bank” pays 10% per annum on invested capital. My template has a little math embedded which converts the annual rate to a daily rate. This allows the player to see, and get excited about, weekly earnings.

Earned Money is Your Money: Most kids have a piggy bank, some kids have side-gigs where they earn spending money. If a player wants to invest that money then they can grow earnings faster.

++

There are two types of spending from the family account.

Investment spending – if the money came from “the bank” then spending approval needs to include Mom & Dad, or another savvy adult.

Earned income spending – Mom & Dad have no veto rights over money the players earn on their own. This allows real world learning to happen. Lending to friends, pain of crappy impulse purchases…

Steps are birthdays, assumed to be Jan 1st in the template. It takes a decade for weekly earnings to exceed weekly allowance. Just like a retirement account, once your earnings start to accelerate, they keep going. Stay invested. Don’t interrupt compounding.

Teaching this to your kids, or grandkids, will change your relationship with money.

The inspiration for this game came from a 2015 post by MMM. What I’m Teaching My Son About Money. We started the day I read his advice. I’m grateful for his sharing.

Keep it simple, be patient, and remember the goal is an emotional attachment to compounding.

I’m back on Twitter, daily – sharing ideas about living better. The focus is health & wellness with financial education for you and your family.

It’s a good place to ask me Qs on my writing.

Capital over and above the needs of current adult family members can be considered multigenerational.

When I was younger, I focused on building net assets. I started saving out of my first paycheck. If a young adult aspires to a family leadership position then this is where they should start.

Looking backwards from 53, the big gains have come from moderating personal choices, particularly associated with assets that don’t produce cash flow. Being an exemplar, here, is the role of senior family leadership.

A better way of viewing financial wealth…

Assets “divided by” current-year spending => gives you a figure expressed in “years-spending”

$2 million of net assets means something very different when…

There’s $2 million of debt sitting on top of it vs being debt-free

Baseline spending is $125,000 vs $250,000

Average age of the earning membership is 35 vs 55

Context matters

Time Horizon also matters!

Family is a dynamic process. I visit for a limited period of time. I change continuously while I’m here.

Years-spending can be compared to life expectancy of senior members and working-life expectancy of earning members.

Each adult member pays their own way.

This is HUGE for long-term returns.

First, because there are no “bad” deals in the family system.

Second, because the high-earners are free to live their lives in a way that most benefits the family system

HINT: teaching young members about life generates a higher return than creating more unearned capital within the family system.

Often overlooked => years left until the youngest members take over their own living expenses. Family is a dynamic process with clear generational shifts (deaths, retirements, careers, graduations, births).

Families don’t need to budget for taking care of everyone, forever. When I started my kids’ allowance, I began teaching the concept of pay-your-own-way. They’ve also been raised with an expectation that they will move out. Living nearby is OK!

As a family, you need to decide the split between future-focused and present-focused capital. Until I was 52, I was totally future-focused. A change we are gradually making is shifting some capital towards present enjoyment. I like to call this capital “recreational.”

If you are going to deploy capital in a “recreational capacity” then consider the nature, and likely impact, of a mistake. Mistakes can come in many forms. Here’s what we’ve learned.

Multiple, smaller bets, with the minimum capital deployed to solve the issue.

Make sure you factor in the cost of ownership, forever. A high cost of ownership can turn a gift into a burden. I know families who spent many years unwinding the financial legacies of wealthy elders.

Remember, the highest form of endowment is the TIME of a parent. How will this choice impact the family member’s time? Don’t tie down your most effective members with admin!

More than comfort, consider how you might be able to deliver “time” to future family members. What is it going to take to assist my children in having the time to be great parents?

Related, my children will have a range of financial “success” in their lives. Constraining myself, today, reduces lifestyle friction in the future (at no cost to their nature-loving Dad).

The role of the family is to support its members in living the lives they choose to live, not to facilitate consumption. My current choices will become the (unconscious) baselines for my grown children.

Adults have a preference for individual family utilization, over collective utilization.

From my dentist, “My kids will use my ski place a lot more… when I’m dead.”

From a friend, “They like to visit… when we’re not there.”

Single geographic locations, with separate living arrangements, have proven a popular way to strengthen families.

From a friend, “Close but not too close.”

Choose peers, and location, with intention.

Our environment exerts a powerful, often invisible, influence on our desires and actions.

Vegas, Aspen, Global Financial Centers… these locations strength traits that lead me astray

Far easier to reach-for-better in Boulder, than struggle with my past.

Where will this location, this choice, take our Human Capital?

What sort of people will we meet?

Availability heuristic, in all things – friends, choices, life partners

Zillow & AirBnB enable families to quickly compare capital-to-own with fully variable access.

I did a quick check for Edwards, CO => $5 million homes available for $7,000 per week in August, the summer peak.

The same capital in VTSAX yields $60,000 per annum.

The smallest real estate mistake is usually 10% in-and-out costs. Even a “money-back” error on a $1 million house has a true cost of at least $100,000 (because you might have to have to hold for a decade).

Wise allocation of time is what grows human capital.

Assets are often a distraction from what needs to be done.

Specific tactics, I’m working on in 2022.

SELL an investment property to enable a market neutral move into an asset the family will use for shared experiences.

At 40, I had too much runway left to finance to make this choice.

At 53, I don’t want to wait until I’m old for (some of) my assets to better serve my life.

It might be tempting to borrow and defer the tax/agents’ fees => recourse leverage is a risk we don’t need to take.

Pre-kids, rolling Nevada with my sweetie. Mobile, flex-time office space that enables me to share experiences with those I love.

An aside… at the back of my mind, I want to purchase an all-season van. I used to own a Sportsmobile and we had a lot of fun.

I worked for a guy who loved cars and a wise investor noted, “It’s better for Ferraris to be bought from carried interest than management fees.”

If you’re going to do something indulgent then: (a) pay down debts, (b) take some money off the table, and (c) limit the size of the outlay.

++

BUY equities at a reduced weighting.

At this stage of my life, I tend to balance “current enjoyment” with “future protection” on a 50/50 basis.

I’m nervous about current valuations. That said, I’ve been that way, FOREVER!

So… stay invested, at a reduced weighting => buy less.

In March 2020 I increased equity allocations to 72% of my Vanguard portfolio.

Allocating additional capital in 2022, I made a reserve for “an investment that benefits the present”…

…then rebalanced to 60% equity allocation.

This reduced the size of the new investment and got me past decision paralysis, driven by a fear of near-term loss.

“Buy less” got me to “stay invested.”

++

HOLD quality local real estate

Years ago, my family purchased a quality piece of real estate where my kids are growing up. Holding the asset, for 10-20 more years, would help my kids get on the property ladder. It’s also a good-enough hedge for an uncertain future.

As I wrote a couple weeks ago, the main financial deliverable for my kids is debt-free education.

If I can hang onto to the real estate asset then they will get a bonus above the debt-free educational start in life.

Simple decisions, good-enough decisions, can free your thinking.

++

WATCH

Be patient, change slowly and focus on sharing experiences with those you love.

You must be logged in to post a comment.