I sold a large real estate asset this week, a residential rental.

There’s an argument that the buyer got the building for free (Twitter thread on backing out land value).

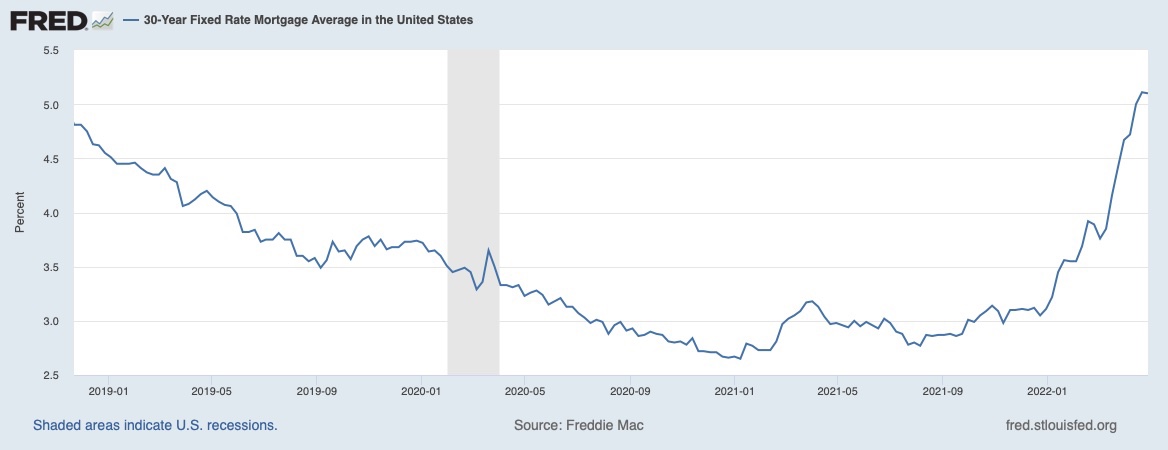

At the closing, my agent (50-ish) shared that the only recession he’d really experienced was 2008/2009. So the next chart is his personal experience with asset pricing.

The above chart is ~20-years of mortgage rate history. If you’re 40-something this is what you lived.

Mostly a one-way bet => falling long rates inflate financial assets.

Back to my sale.

I sold for a three reasons:

- At 53, my life is changing. The window of what I need to finance is less and less. I have begun a strategic shift towards creating the life I want to live in my 60s.

- Real Estate is lumpy, we don’t have the ability to incrementally rebalance. I wanted to reduce exposure before making any additional purchases.

- The sale was valued at 43 years gross rental income (2.3%). Cash proceeds, after tax, were 64 years net rental income (1.6%).

Here’s the last 1,000 days in the mortgage market.

The real estate market is like a super tanker, it takes a long time for momentum to shift. After the 2008/2009 recession, non-foreclosure prices didn’t adjust until the middle of 2010.

- Prices move at the margin => the marginal buyer had a strong tailwind through the pandemic, that has changed in 2022.

- There will be an impact of the near-vertical move in rates this year => initially, we will see this in markets that require loans to complete.

- The scale of “the impact” is unknowable and complicated by supply shortages of re-sale houses and for new build.

- Prices are being supported by rapidly rising cost-to-build and cost to renovate/remodel.

Lots going on – I can make a case for +25% and -25%.

At 53, taking 64 years-equivalent cash-flow off the table, in a rising rate environment, is a decision I’ll be able to live with regardless of future outcome.

You must be logged in to post a comment.